The article tells what documents are needed to refinance a mortgage, explains the intricacies of the legislation.

Refinancing a mortgage at VTB 24 or any other financial institution means issuing a new loan to pay off an old loan.

It is especially beneficial to refinance when the interest rate changes.

Example, Grigorieva took out a loan at 12% per annum. A year later, the interest rate fell and amounted to 9%. In this case, it makes sense to refinance in order to repay the loan already on more favorable terms.

There are other reasons for a credit reset:

- change the repayment period of the loan;

- change the payment currency (especially relevant for currency mortgages);

- change the loan amount.

A credit institution may change the subject of collateral.

Example. The Stanovovs bought an apartment for their son. The mortgage under the contract is their house. Now they have decided to improve their living conditions and sell the house. To do this, you will have to change the subject of collateral. The encumbrance will be removed from the house, then it will be possible to conduct transactions with it.

The issue of mortgage refinancing can be resolved in your financial institution or choose another bank.

Mortgage refinancing

To refinance a mortgage at Sberbank, you must first agree with the company's management and collect documents.

Lots of companies offer credit reloading. Among them are Sberbank, VTB-24, Alfa-Bank and many others. To approve the transaction, the borrower must insure his life and the object itself.

Is there any benefit from the deal?

It is necessary to clarify in advance with the refinancing institution how much the paperwork will cost.

6 items of expenditure:

- property valuation;

- payment for the removal of the encumbrance;

- payment for re-registration of the right;

- insurance payment;

- bank commission for issuing a loan;

- fees for wire transfers.

When Can Renewal Be Denied?

The question of what documents are needed for official mortgage refinancing will not have to be decided if the financial institution has banned such operations.

Some banks prohibit early repayment of the loan. True, such decisions can be challenged in court. Therefore, most banks give the go-ahead for early fulfillment of obligations.

Sometimes re-registration is not allowed due to the fault of the client himself. For example, credit debt or outstanding debt impedes a credit reset.

If the borrower's income has decreased or he has lost his job, the bank may also refuse to issue a loan. In this case, there are doubts about the solvency of the borrower.

The subject of collateral may also not suit the bank. The requirements for the degree of deterioration of the object differ. One bank may approve the purchase of an apartment in a house built in 1975, while for another bank such an object may be too old.

Important! You need to be prepared to provide additional security. At the time when the encumbrance is removed, it is necessary to secure a new loan. If the borrower has nothing for the soul, then it will be quite problematic to do this.

In any case, you need to get up-to-date information from bank employees.

Sberbank is a reliable financial institution, so many citizens want to make on-lending there.

7 benefits of refinancing:

- The ability to collect several loans issued in various financial institutions in one loan.

- Simplify debt repayment. There will be a single payment date, one invoice is issued.

- No need to collect certificates from other companies about the balance of the debt.

- The consent of the primary lender is not required for the next loan.

- Getting a benefit. The amount of contributions will decrease, which means that you will have to pay less.

- Opportunity to receive additional cash for personal expenses.

- Low loan rate.

Conditions may vary depending on various companies Therefore, it is desirable to collect the necessary information in advance.

Pitfalls of refinancing

The credit reset has positive and negative sides.

5 cons of the deal:

- The borrower will be checked again. After all, the company must make sure. That he, indeed, will be able to fulfill his obligations.

- Again, you will have to decide what documents are needed for re-registration.

- The item may not fit. When it comes to car loans, this situation is especially relevant. Requirements to vehicles may differ greatly.

- Additional costs will have to be incurred. For many borrowers, every penny counts, so additional spending is highly undesirable.

- Probability of getting rejected. Such a possibility cannot be ruled out. In case of refusal, the commission for consideration of the application will no longer be returned.

In some situations, it is no longer necessary to talk about pluses and minuses. When creditors are already literally knocking on the door, and there is nothing to pay, you have to look for a way out of the situation.

How to make a deal

You need to act consistently in order to refinance in VTB-24, Sberbank or another company.

Procedure:

- Apply.

- Wait for an answer.

- Collect documents for the apartment.

- Wait for approval and specify the date of the transaction.

- Sign a mortgage agreement and register it.

- Get money.

- Pay off the original loan.

- Get confirmation certificates.

It is important to submit debt repayment documents no later than forty-five days from the date of payment.

After the primary loan is repaid, the financial institution will be able to reduce the interest rate on the loan.

Borrowers should be aware that property deduction under Art. 220 tax code they can't.

Requirements for the borrower

Each company sets its own requirements for borrowers.

3 general conditions:

- age from 18 to 55 years;

- availability of registration in the region where the banking unit is located;

- permanent job for six months.

If a co-borrower appears in the primary contract, then he is also responsible for refinancing.

Sberbank installs preferential terms to their payroll clients.

Required documents

There are documents that the borrower must provide:

- Completed application form.

- Passport.

- Certificate of temporary registration, if the citizen is temporarily registered.

- Income statement.

- Copy work book.

- Details of the original loan agreement:

- date of signing and serial number;

- the amount of the monthly payment;

- loan currency;

- payment details of the original creditor.

- Payment scheme.

After the application is approved, the property documentation is submitted.

Summary

Credit reloading makes it possible to repay a loan that was issued on unfavorable terms. The issue of refinancing is especially relevant for foreign currency mortgages and those who have taken a loan with an unfavorable interest rate.

Thanks to refinancing, it is possible to significantly improve lending conditions for more favorable ones by repaying the old cash loan with a new one, issued in another bank.

As a rule, clients decide to refinance if such a program involves a lower interest rate, a more convenient loan repayment period, and other favorable conditions.

The first step in obtaining refinancing should be the submission of an appropriate application to the selected bank. We will describe the features of the procedure below.

How to apply for loan refinancing?

In order for an application for on-lending to be approved, the borrower must meet the basic requirements of the bank. Therefore, before sending an application, you should familiarize yourself with the basic conditions of a potential lender. As a rule, these parameters are similar for many credit institutions. This:

- Age 21 and over.

- Having a formal job. Such information must be confirmed by an appropriate entry in the work book.

- stable wage (monthly payment credit should be no more than 50% of salary).

- Citizenship in Russia (Russian banks do not offer refinancing to foreign citizens, but they can draw up such an agreement in foreign banks, for example Deltacredit. details)

- Registration at the place of residence on the territory of our country (temporarily or permanently).

Through a bank

The client should contact the office of the chosen credit institution and write a statement. The form is issued on the spot, and you only need to have a passport with you.

The bank considers the application within 3-10 working days and makes a preliminary decision. Further, the client must bring the entire package of documents and wait for the same period (sometimes longer) before receiving a final answer.

To reduce the time for consideration of the application and making a decision on it, you can familiarize yourself with it in advance and come to the bank already with a complete package for writing an application. This will allow you to get not a preliminary decision, but a final one.

Online

Today, most banks strive to simplify the procedure for interacting with customers and make it as comfortable as possible. So the presence of an online resource where there is last news, Access to personal account and other important options make the process of obtaining the necessary information almost instantaneous.

If you want to refinance a loan, just go to the official website of the selected bank and fill out an online application. This can be done at any time of the day, which is very convenient, since there is no need to adjust to the lender's work schedule and look for time to go to the bank. The term for consideration of online applications is shorter than when they are submitted at the bank and is 1-3 days.

It should be noted that the desire for refinancing must be approved not only by the bank in which it is supposed to receive new loan, but also by the financial institution whose loan is supposed to be closed ahead of schedule. If the relevant consent is not in the text of the loan agreement, it must be obtained on a separate documentary form.

The application form is standard and includes the following information:

- Surname, full initials of the potential borrower.

- Day, month, year, place of birth of the client.

- Identification code.

- Contact details:

- address of residence and registration,

- email box,

- phones: home, mobile, work.

- Contacts of close relatives.

- Information about the place of employment and the amount of monthly income.

- Information about the property owned by the future client.

When contacting the bank, the form for filling is issued according to the passport. When applying online applications you just need to fill in all the fields.

Sample application for refinancing a loan

Deadline for consideration of an application for refinancing

After the online application for refinancing is sent to the credit institution, potential borrower You will be asked to wait 1 to 3 days. When submitting a questionnaire through a bank, the deadline can be extended up to 5 business days.

What to do after the application is approved?

After receiving information that the loan is approved, the client should come to the bank branch with necessary documents for the execution of the refinancing agreement.

Required documents for refinancing a loan in another bank:

- Documentary proof of identity in the form of a passport.

- A copy of the work book, certified by the organization in which the borrower is employed.

- Certificate of income (mainly 2-personal income tax).

- A copy of the loan agreement to be refinanced, with all existing attachments.

- Expressed documentary consent of the bank - creditor to early repayment of the loan (in the absence of such in the body of the loan agreement).

- Extended statement of loan account opened to the client for loan repayment.

- Help from financial organization, confirming the absence of delays in the payment of planned (urgent) debt.

Is it possible to reapply if denied?

If the bank refused to refinance for good reasons, you should not despair. Re-applying for refinancing is possible, it is only necessary to eliminate the factors that caused such a refusal.

The time interval that must be observed when submitting several applications is not established by law. However, experts advise not to send a second request for refinancing earlier than 30 days after the bank's refusal.

Refinance the current Housing loan under more low interest You can either in your bank or by contacting another. What is on-lending, what are the costs involved, which bank is better to contact, is it profitable, and what stages does it include, we will consider in detail in the article.

Mortgage refinancing concept

A mortgage loan for the majority of average Russian families today is practically the only way to buy their own home. And many people took advantage of this opportunity a few years ago. The market does not stand still, and the conditions of many banks are now much more favorable than even a couple of years ago. Naturally, many borrowers would like to refinance on more favorable terms. It also benefits banks. Mortgage in the credit line of banks is one of the most profitable products. Therefore, most of them, in order to increase profits, try to sell as much as possible. mortgage loans. One of the tools to attract mortgage borrowers is the refinancing of mortgages from third-party banks.

Mortgage refinancing or on-lending is the registration of a mortgage in one bank in order to repay the debt obligations of another bank on more attractive terms (at a lower rate, with a shorter term, or with the issuance of an additional amount in cash).

Is it profitable to refinance a mortgage?

At first glance, refinancing seems profitable banking product. The lower the rate and term of the loan, the less you will overpay for your housing, you will be able to reduce the monthly payment, especially if the loan was issued for a long period.

Based on statistical data, it is worth thinking about transferring a mortgage to another bank if the difference in rates is at least 2-3 percent.

But apart from interest rate other costs associated with refinancing should also be taken into account. These include:

- At the stage of application, the amounts are insignificant, 50-100 rubles for issuing a certificate of balance loan debt(not charged by all banks).

- Small expenses in the preparation of documents for collateral real estate (certificate from the BTI, registration certificate, etc.).

- New valuation report on collateral (about 6-7 thousand rubles).

- Payment of the state duty for the removal of the encumbrance and registration of a new pledge.

- Expenses for execution of an insurance contract in favor of a new bank. The calculation of the amount is individual. The minimum rate is from 0.2% of the value of the collateral, but it should be borne in mind that only insurers accredited by the bank will do. In some cases, one can conclude additional agreement to already current policy on the change of the beneficiary, or terminate the contract ahead of schedule. This question It is better to discuss with the insurance company in advance.

- When refinancing, in most cases, the right to tax deductions for the purchase of real estate and mortgage interest is lost.

- Notary fees.

Thus, the answer to the question of the profitability of on-lending will depend on the specific conditions of each borrower.

Usually, with a long term of the initial loan, a small number of payments already made, a difference of 2% in rates, the associated costs pay off in the first year. If at the same time the right to tax deduction implemented in full, then it is definitely worth deciding on refinancing.

Bank your own or someone else's?

Of course, if there is such an opportunity, then initially you should contact your creditor bank with a request to reduce the interest rate.

Apart from financial costs for the revaluation of property and re-registration of collateral, refinancing involves a large investment of time and effort. Therefore, refinancing in your bank is most convenient.

But it is not profitable for banks. Reducing the rate on loans already issued will reduce the planned profit. That's why current programs refinancing for own clients is a rarity.

Refinance with current lender

If the current lender does not have a mortgage refinancing program for its clients, but the current rates are already lower, or, in general, there has been a decrease in interest on the market, it is necessary to write an appeal addressed to the head of the credit organization to consider lowering the rate. In the appeal, indicate your data and the data of the loan agreement. The review period is usually not more than 30 calendar days.

If the policy of the bank and the terms of the agreement provide for the possibility of revising the interest, then a positive decision is possible.

In 2017, Sberbank was one of the first in Russia to lower mortgage rates to 7.25% and launched a program to refinance loans from third-party banks at a rate of 9.5% per annum. At the same time, this program did not touch its clients.

Reviews on the banki.ru portal testify that many borrowers, in response to their appeals, have had their rates reduced. Basically, under contracts concluded a very long time ago or at the beginning of 2015, when rates skyrocketed to 14.5%.

How to motivate your lender

The fact is that according to the standards of the Central Bank of Russia, refinancing your own loan is equated to restructuring and entails additional costs to increase bank reserves.

The only way to motivate can be an approved application for refinancing in another bank.

A similar appeal is written, as in the first case, but with an attached copy of the positive decision of the new creditor on the application. Practice shows that the chances of an affirmative answer increase.

Mortgage refinancing in another bank

If you refuse to reduce the rate in your bank, you can always contact another or even several.

Applying to another bank involves going through the procedures for approving a mortgage, collateral, transferring money to repay a new loan, re-registering collateral rights, an unsecured period, and concluding a new insurance contract. Let's take a closer look at each of these stages.

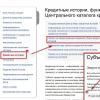

Mortgage loan conditions

| Bank | Interest before mortgage registration and loan repayment | Interest after registering a mortgage and repaying a loan | Term | Sum | Pledge | Requirements for the borrower |

|---|---|---|---|---|---|---|

| Sberbank | 11,5 % | From 9.5% | Up to 30 years old | From 1 to 7 million rubles, but not more than 80% of the housing appraisal | Apartment, house, townhouse, room, plot of land and residential building on it, part of the house, apartment | Russian citizens, 21 - 75 years old (by the time of debt repayment), half a year at the current place of work, a year of experience over the last five years |

| VTB 24 | From 9.45% for the entire loan term | Up to 30 years (according to 2 documents up to 20 years) | Up to 30 million rubles, but not more than 80% of the housing valuation (50% according to 2 documents) | Citizenship of the Russian Federation, registration in the region where the banking unit is present, permanent income | ||

| AHML | Before registration: no After: 9% - the loan is less than half of the value of the appraisal; 9.25% - from 51% to 70%; 9.5% - from 71% to 80% (The rate increases by half a percent if the income is confirmed not by 2-personal income tax) | 3 to 30 years old | 300 thousand rubles - 20 million rubles. for Moscow, Moscow Region and St. Petersburg; 300 thousand rubles. - 10 million rubles. for other regions | apartment or non-residential premises. In the case of an object under construction - a pledge of rights of claim | 21 - 65 years old (by the maturity date), half a year at the current place of work (IP - 2 years without losses) | |

The requirements for the previous loan are the same for all offers:

- action for at least six months:

- lack of restructuring;

- without delays current and past.

In case of cancellation of the borrower's life and health insurance contract, 0.5 - 1% is added to the rate. Collateral insurance is a must.

Registration procedure

To apply for refinancing, you must submit to the selected bank loan application with the required documents.

Primary package of documents:

- A completed application form for all borrowers (official spouses automatically become co-borrowers, even without taking into account solvency).

- Passport and any additional document.

- Salary information.

- Scanned copy of the labor with certification (if certified by proxy, then a copy of the document on the delegation of authority).

- Certificate of the balance of loan debt (valid for 10 days).

- Requisites for repayment of the current loan.

- Certificate of absence of overdue payments (not everywhere).

- Loan agreement, repayment schedule (upon request).

After a positive decision within 3 months, you will need to provide documents for bail:

- Ownership documents.

- Extract from USRN.

- Evaluation report.

- Registration certificate.

- The consent of the spouse to the transfer of property as a pledge, certified by a notary.

- Information about registered residents.

The final list may be supplemented at the discretion of the bank. It usually corresponds to the standard package for accepting collateral real estate.

When the bank agrees on the subject of collateral, a loan agreement is signed. The money is transferred to repay the old loan.

Re-registration of pledge

The re-registration of the pledge does not take place at the same time, that is, first the encumbrance of the first bank on housing is removed, and after that the registration of a new pledge takes place. Usually new bank give it 2 months.

After the loan is fully repaid, it is necessary to request from the old bank the following documents:

- certificate of full repayment of credit obligations;

- mortgage agreement;

- mortgage with a note about the full closure of the loan, including fines and penalties;

- a bank power of attorney in the name of the client on the possibility of representing the interests of the bank.

Actions for re-registration of collateral are carried out by Rosreestr. It is more convenient to use the services of the MFC.

To cancel the deposit at the MFC, the following documents are required:

- Passports of adult owners, birth certificates of registered children.

- Certificate of ownership.

- Documents from the bank (valid for 30 days).

- Those documentation for housing.

- Certified consent of the spouse to cancel the bail.

- Statement.

- Receipt for payment of state duty.

Processing time is 3 business days. As a result, a new certificate of ownership is issued with the absence of a mark of encumbrance.

The next step is to register a new pledge.

Documents required for the MFC:

- Bank documents confirming the authority of the representative.

- Mortgage documents (loan agreement, DKP or DDU, pledge agreement, mortgage).

- Housing documents (assessment, property, BTI certificates, technical documentation).

- Application for registration by the bank and by the owner.

- Copies of passports of all participants in the transaction.

- Receipt for payment of state duty.

The registration period is 5 business days.

Important! It is necessary to add 3-4 days to the official deadlines for processing documents at the MFC courier delivery documents. When receiving documents from the MFC, be sure to check the certificates for errors and typos.

Free period

The unsecured period is the period of time after the issuance mortgage loan until the registration of the mortgage by Rosreestr. Its duration is about 2 months, subject to deadlines by all parties.

This period is considered the most risky for the bank in which refinancing is issued, since there is no collateral. Therefore, the loan rate for this period increases by about 2 percent.

Obstacles

You will not be able to refinance your loan if:

- it has already been restructured, overdue payments, refinancing;

- V loan agreement there is a moratorium on early repayment (possibly in old contracts). Starting from 2011, it is prohibited by law to prevent early repayment of loans;

- bad credit history, insufficient level of income, non-compliance with other criteria of the bank;

- housing does not fit the conditions of the pledge of the new bank.

Mortgage on-lending risks

Refinancing risks:

- If the bank refuses to issue a loan, the costs of preparing documents, including collateral, will not be compensated.

- duration of the procedure and big number bureaucratic moments can increase the term for re-registration of collateral, and, accordingly, delay the moment of setting a low rate.

How to transfer a mortgage to another bank with a better interest: mortgage refinancing step by step

Summarizing all of the above, here is a step-by-step algorithm for refinancing a mortgage:

- Choosing a bank with suitable conditions.

- Collecting documents and submitting an application for consideration to the bank.

- With a positive decision of the bank - preparation of documents for collateral.

- If the bank has arranged everything on the pledge, then a deal is appointed.

- Submission of documents on home insurance (some banks can provide later).

- Signing a mortgage agreement and transferring money to the old bank to repay the loan (you must first submit an application to your bank for full early repayment loan).

- Loan repayment and request for documents to remove the encumbrance.

- Submission of documents for the cancellation of bail.

- Submission of documents for registration of pledge in favor of a new bank.

- Submission to the bank of documents confirming the registration of collateral.

- Setting a low interest rate by the bank.

- Annual provision of payment documents for the extension of the insurance contract (if necessary).

Refinancing a mortgage is not an easy process that will require not only material investments but also a huge investment of time and effort. All this makes sense if in a particular case the benefits significantly exceed the costs. Therefore, it is very important to calculate and weigh everything in advance.

Hello,

With you Dmitry Ovsyannikov and again questions from the forum of the portal "".

A man under the nickname Serggg writes: "Hello. I took out a mortgage two years ago secured by existing housing on new apartment in UralSib, but since Since they closed all their branches in my region this year, I decided to transfer (refinance) the mortgage in Sberbank. I submitted an application to Sberbank, began to collect documents - I was previously agreed on refinancing.

As a result, an employee of Sberbank calls me and says that Sberbank cannot accept an already encumbered apartment on bail and they only need an unencumbered apartment on bail.

Judging by banking practice, the scheme is simple as "3 kopecks". Sberbank transfers the rest of my debt to UralSib, after that I go to the registration chamber (Justice), remove the encumbrance and immediately burden it in Sberbank.

Tell me, does Sberbank have the right to refuse to provide me with a pledge of a burdened apartment? (I understand that he can, but he must refer to the norm of the law?) ”

Sberbank should not refer to the norm of the Law.

Why?

Because while you are nobody for Sberbank.

Your relationship as a client and the bank begins only from the moment of signing the loan agreement.

Up to this point, yes, you have submitted an application form to Sberbank. But this is, so to speak, a "one-sided deal": you have declared your intention. The bank is reviewing this form. He can, at the stage of study, make any decision: approve a loan for you, refuse: refuse for one reason, refuse for another reason ...

Sberbank, when refinancing (today there is such a program), it insists that the primary creditor bank agree to such refinancing. It is not a fact that Uralsib will agree to the subsequent mortgage of the apartment.

Most likely it won't.

That is, you applied to the wrong bank. In order for you to refinance, you need to apply not to Sberbank, but to some other bank: to the bank where the scheme that you described as “simple as 3 kopecks” is possible. Where the bank issues money and does not require (at some time) a mandatory pledge of an apartment. That is, a pledge of an apartment can happen, but it can happen with a slight delay: in 3, 4, 5 months.

There are such banks.

But this is not Sberbank.

You need to apply to those banks that do not require a subsequent pledge during refinancing: they do not require the provision of documents from the primary lender for a subsequent pledge.

There are such banks, but I don't know if they exist in your region.

Thank you for your attention.

I was with you, Dmitry Ovsyannikov and the project "".

If you have questions about mortgages or real estate, ask them at.

Mortgages are a heavy burden. If a person manages to find a bank that will issue a loan on more favorable terms, it makes sense to refinance to reduce the monthly payment and overpayment for the entire period. This procedure is called mortgage refinancing. It involves closing a loan in one bank and “opening” it in a new one, but on more favorable terms. How to refinance a mortgage, and what difficulties will you face?

Mortgage refinancing - when, why and to whom?

In fact, refinancing is the right of the borrower, which is enshrined in the Mortgage Law (Chapter 7). The legislator clearly indicates that collateral (real estate) can be transferred to secure a loan to another creditor.

Almost everyone big bank can offer its clients a refinancing program mortgage loan. Since the competition in banking high, products in the area mortgage lending different favorable conditions for borrowers.

Individuals who have taken out a loan high stakes, before refinancing a mortgage in a third-party bank, you can try to reduce the terms of the current agreement. It is unprofitable for the bank to lose a conscientious payer, therefore, most likely, it will be possible to reach a consensus. For example, VTB willingly reduces the inflated interest rate to its current customers if they meet certain conditions. If it is not possible to agree, you can safely apply for refinancing to other financial and credit institutions.

When you may need to refinance:

- The borrower cannot secure the loan obligation on the same terms - loss of a job, birth of children, etc. In such a situation, it is worth preparing the ground for refinancing in advance. Write an application to the bank about the changed living conditions and ask to restructure the debt or defer mortgage payments for some time. If you were refused, ask for a change in the terms of the contract (mortgage refinancing).

- The man managed to find a bank that offers more than low rate on a loan - even a 1.5-3% difference can reduce the monthly payment by several thousand rubles.

- The loan was issued in a foreign currency and, due to the growth in the exchange rate, the payment became too large - you can look for a loan in rubles (VTB24 Bank and Alfa-Bank refinance such obligations - the conditions are individual for the borrower).

- The borrower has improved financial position- in such a situation, refinancing will help to significantly reduce the overpayment. This happens as a result of favorable interest on the loan, and reduce the loan term. If a decision is made to issue a loan for a shorter period, most banks "encourage" such payers and reduce the mortgage interest by an average of 0.5 - 1%.

Most likely, your bank will "resist" refinancing your mortgage in another financial structure. True, many banks themselves are ready to refinance you so as not to lose a client. How to proceed in this case:

- Write an application to the bank where you have a mortgage with a request to refinance an unfavorable loan. In such a situation, you can save a lot on additional costs, which will be discussed below. An operation within the bank will not require special costs, because the structure has already evaluated the apartment or house, it has all your documents and income statements. In some situations, they may be asked to prove that your situation has worsened - take a new income certificate or provide tax return for the last reporting period.

- You were refused - it is worth defending your intention. Look for a bank where the interest is lower and provide this information. Still do not agree - we are preparing for refinancing in another bank.

New loan The op will carefully check your story, and if it is "doubtful", you should not expect a positive outcome. It will significantly reduce the chance of refinancing at a bank if you have already applied to another bank and were refused there.

Where to apply for a mortgage loan?

First of all, analyze lending rates offered by banks. If your mortgage is issued, for example, at 16-18%, then it makes sense to contact banks: VTB, UniCredit Bank, Alfa-Bank, Sberbank, MTS Bank, Rosbank, Gazprombank. These structures offer to refinance you on terms reduced rates– from 9.5% per annum. In cash, this difference is quite significant, and the programs of banks are very flexible. Please note that banks will not give you 100% security deposit, but 70-90%.

Refinancing for a new bank is, in fact, opening a new loan. And this means that you will have to go through the whole procedure again to confirm your solvency and more. How it all happens:

- An old contract is provided for analysis by creditors, receipts for payments, a certificate of no debts to the first bank.

- A new contract is concluded in the selected bank.

- The collateral must be insured, and an independent assessment of the property will also be required. Banks have their own accredited experts, so the price of the service can be much higher than that of independent specialists. The life of the borrower is insured.

The first version of events - three parties sign (the old bank, the new bank and the borrower) a tripartite agreement. This document will become a pledge of the second stage, but only on condition that the old lender has agreed to refinancing. The new bank then rolls over the full amount to pay off the mortgage, making sure the funds are used for their intended purpose. After that, the old creditor is obliged to remove the encumbrances from the property in the register of prohibitions and the pledge (apartment, house) must completely pass into the possession of the new creditor. The new bank, in turn, again imposes an encumbrance on the property and becomes the mortgage collateral holder.

If your bank does not agree to refinancing, another scheme is applied:

- The full amount of the mortgage (balance in the old bank) is transferred by bank transfer to the lender.

- The borrower writes an application for early repayment of the mortgage.

- The old creditor removes encumbrances (the procedure lasts 1-2 months).

- The pledge is transferred to a new lender and you are already issued a new mortgage loan on more favorable terms.

But in such a situation, the lending bank must receive a guarantee, a new pledge for a period while the encumbrance is in effect and, in fact, the apartment belongs to the old bank. The collateral may be other property or real estate of the borrower.

There is none - for this period you can increase the interest on the loan by 2-3 points. But Rosselkhozbank is ready to take a risk. It does not require collateral for the period of removal of the encumbrance and does not increase the mortgage rate, the maximum credit limit in this case, 5 million rubles. A package of documents required for collateralized real estate can be submitted to Sberbank after refinancing is approved, but no later than 90 days later.

Remember that in any case you will have to pay for such a "reboot", but if you are offered good conditions- the costs will quickly pay off.

Mortgage broker - when should you use the services?

This is another option for refinancing a bad mortgage. The bottom line is that you don't have to wait until your old mortgage is paid off. A new loan will be issued even before the old one is completely closed. The role of a mortgage broker - he will become a guarantor to the new bank for an "unsecured" lending period, as long as there is an encumbrance and it is reflected in the register. It's about about 1-2 months, during which the old bank will remove restrictions.

Also, a specialist will help in the collection and design necessary papers, will take away profitable offer within the framework of refinancing, will promptly resolve emerging disputable issues, will independently interact with the bank.

The cost of intermediary services is determined as a percentage of the loan amount. Today, this value averages 1-5% of the transaction price. What's with the benefit? If your monthly payment decreases with new mortgage for 5000 - 6000 rubles. monthly, it's worth it.

On-lending conditions - documents and costs

You have found a new bank and agreed on the terms with the old one - you will have to go through the long-forgotten mortgage procedure again! And here you can not do without extra costs. What to prepare for:

- New collateral appraisal - as a rule, each bank has its own accredited appraisers. Their services will cost from 3,000 to 10,000 rubles.

- The commission associated with the refinancing of the loan - each bank has its own, on average 1 -1.5% of the mortgage balance. This fee, according to the conditions of a particular bank, may not be.

- Transferring money to another bank non-cash payment- from 1 000 rub.

- New insurance contract. The amount of the insurance premium directly depends on the size of the loan.

- Payment (state duty) for the removal of encumbrances from the property.

- Assurance mortgage agreement at the notary - although this rule is not mandatory, many banks require you to go through the procedure.

In addition to the mandatory procedures, it is necessary to submit identification documents, a certificate of income, a copy of the work book, registration documents for an apartment or house, an old mortgage loan.

Mortgage refinancing is a profitable undertaking if you find a bank that offers good interest. True, it is worth remembering that the main condition for successful on-lending is a “clean” history.

The essence of the restructuring of credit debt

The process of restructuring credit debt includes changing the terms of the financial contract. This reduces the client's burden and reduces the amount of the loan payment. The difference between restructuring and refinancing - change credit conditions The contract takes place at the original creditor bank. The borrower submits an application for restructuring to the bank that issued the loan.

Reasons for the on-lending process:

- Offensive insured event.

- The emergence of negative situations for the borrower is determined by the inability to pay the loan debt in full.

Changing the terms of credit is the best option for solving customer problems. The banking organization goes towards people, pursuing the following goals:

- The quality of the loan portfolio.

- No litigation.

- Return of credit funds

Credit debt restructuring is available to clients of any age category. Usually, banks welcome the desire of the borrower to correct the negative status in front of the financial structure and continue to repay the loan.

Pros of restructuring

- Registration of a new loan agreement with an increase in the loan term, which reduces the amount of the monthly payment.

- It is possible to provide a new interest rate, lower.

- Availability of a convenient payment schedule.

The actions of the bank to repay the debt in cases where the client does not apply for restructuring, but continues to stubbornly hide from payments:

- Introduction of strict repayment conditions.

- Calculation of penalties.

- Cooperation with collection services.

- Appeal to the court.

- Litigation statistics show that debt relief is rare.

The borrower expects to receive easing conditions from the bank. The following possibilities open up:

- Maintaining a positive credit history.

- No litigation.

- Saving.

- Getting rid of default (minimization of payments according to the schedule of the loan agreement).

- No penalty payments.

- Protection against forced collection of debt on a loan.

The lending process is regulated regulations. Registration of documents takes place in accordance with the legislation of the Russian Federation.

Refinancing by type of lending

Job banking system includes many types loan products: consumer lending, trade credit, mortgage, car loans.

For example, restructuring consumer credit: in this case, the terms of the loan agreement are revised. since there is no collateral and guarantors, the conditions for the term of the loan and sometimes the interest rate are usually revised.

Mortgage lending for restructuring is a more time-consuming process. Russian legislation has decided to support mortgage borrowers. This was the reason for the introduction of a special restructuring program, the creation of the structure "Agency for Restructuring housing loans For separate category debtors." The scheme of work of the Agency:

- Providing grace period borrower.

- The repayment of the mortgage occurs at the expense of the monthly tranche of the company.

The essence of the stabilization loan is to provide the client with support. The loan is provided:

- To pay for mortgage insurance.

- To recover penalties.

This process avoids the loss of property. The client undertakes to improve his financial condition within the grace period.

Restructuring a car loan is carried out using simplified methods. The borrower applies to the bank with an application. The bank offers conditions for on-lending.

The repayment period is extended, sometimes the interest rate is reduced - the restructuring option is available for loyal customers.

For persistent defaulters, more and more often, the bank confiscates the car as a debt - this covers part of the principal debt, and the client pays the rest.

Types of restructuring

Appeal to the bank indicates the desire of the client to repay the loan debt.

There are the following types of restructuring:

- Loan extension. The essence of this process is characterized by an increase in the term of credit. Reduced monthly payment. The downside of the transaction can be attributed to an increase in the final overpayment on the loan. Preliminary calculations are held loan officer and agreed with the client.

- Currency replacement in lending>. Rate growth foreign exchange involves an increase in the cost of a loan when it is paid in ruble payments. This option is unfavorable for customers. Transfer to Russian ruble allows you to soften the terms of debt repayment.

- Credit holidays. The bank provides the client with the opportunity to pay only the body of the loan for a certain period of time. Interest for this period is not accrued or paid, additional overpayment for credit debt No. This option is especially attractive to the borrower. General provisions credit holidays determined by the conditions of specific banking organizations.

- Lowering the interest rate. The restructuring program, which results in a rate cut, is carried out for customers with a positive credit history.

- Combination of prolongation and currency exchange. Combining types of restructuring leads to a larger overpayment. the currency is recalculated at the exchange rate of the Central Bank on the date of the conclusion of the new contract. Fixed debt in new currency, the interest on the loan is set corresponding to the given currency, the loan term is changed, the TIC is calculated taking into account the new conditions.

Algorithm for changing the terms of credit debt

Restructuring is the best option for solving problems with repayment of a loan, when it is important to reduce the monthly payment to the optimal amount for resuming regular monthly payments.

Procedure for changing credit obligations:

- Collection required documents(passport of a citizen, application form, work book, certificates from the place of work, consent of the spouse (a) to change the terms of the loan).

- Loyalty banking organization. financial structure obtains evidence of the bankruptcy of the borrower.

There are a number of conditions under which restructuring is carried out:

- Decreased customer income.

- A loss additional source arrived.

- Care leave to care for the disabled.

- Conscription.

- Severe illnesses.

- The onset of insured events (death, disability).

The main provisions of the restructuring

The advantage of on-lending is the free implementation of this operation. An exception would be a mortgage loan. This case involves the payment of related costs: notary services, re-registration of the loan agreement. The disadvantage of restructuring is a large final overpayment. This is due to an increase in the loan term and this, of course, is not in favor of the borrower. However, it should be understood that the impossibility of paying the loan under the old conditions arose through the fault of the client. Exception: the occurrence of an insured event. But the undoubted advantage will be a reduction in the monthly payment, which will allow you to pay painlessly and on time. Therefore, loan restructuring is the best solution to problems.