The authorities of the subject can completely exempt organizations from paying tax on movable objects. For example, in Moscow and the Moscow Region, the tax on movable property canceled since 2018. We will tell you how long you can apply the new rates and how to pay tax.

From January 1, 2018, new rules on property tax are in force. The amendments affected movable assets that companies have acquired since 2013. If back in 2017 such objects were exempt from tax, now you have to pay for them in regional budget. But such an obligation may not exist if the local authorities have exempted this property from tax.

There is no longer any federal personal property tax credit. But the regions received the right to independently introduce benefits on their territory (clause 1, article 381 of the Tax Code of the Russian Federation). The tax on movable property must be paid at a rate of 1.1% from 2018 if the regional authorities have not approved their own. The Federal Tax Service announced this in a letter dated December 20, 2017 No. BS-19-21/327 in response to a private question.

Tax on movable property from 2018 in Moscow

From January 1, 2018, the decision on exemption from tax on movable property of organizations is made by regional authorities. According to the norms of Federal Law No. 335-FZ of November 27, 2017, a constituent entity of the Russian Federation has the right to issue a law on the application of tax benefits on movable objects on its territory. If there is no such law, the rates for movable property cannot exceed 1.1% in 2018.

The Moscow Government received many requests from organizations and individual entrepreneurs with a request to maintain a zero tax rate on the property of organizations in Moscow from 2018. As a result, amendments to the Law of Moscow "On the tax on property of organizations" were adopted, that is, from 2018, the zero rate of tax on movable property was retained.

As a result, the Moscow City Duma adopted the Law “On Amendments to Article 4 of the Law of the City of Moscow dated November 5, 2003 No. 64 “On Corporate Property Tax”. The document extended the zero rate of tax on movable property for 2018.

Article 4 of Law No. 64 lists the existing benefits. Organizations in relation to movable property specified in paragraph 25 of Article 381 of the Tax Code of the Russian Federation have been added to the number of beneficiaries.

Law No. 4 applies to legal relations that arose from January 1, 2018, and becomes invalid from January 1, 2019. That is, the tax on movable property in Moscow has been canceled for one year so far.

The tax rate on movable property in 2018 in Moscow- 0%

Vladimir Efimov, Minister of the Moscow Government, Head of the Department economic policy and development of the city of Moscow, on the tax on movable property of organizations in the capital from 2018:

Tax on movable property from 2018 in the Moscow region

In the Moscow region in 2018-2020, in relation to movable property accepted by the organization from January 1, 2013 for accounting as fixed assets, the rate of 0% is also set (see table). Corresponding amendments were made to the Law of the Moscow Region dated November 21, 2003 No. 150/2003-OZ "On the Property Tax of Organizations in the Moscow Region". The document entered into force on January 1, 2018.

The tax rate on movable property in the Moscow region in 2018-2020- 0%

tax rate in relation to movable property in the Moscow Region, registered as fixed assets from January 1, 2013, is set at 0% in 2018-2020, with the exception of the following objects of movable property, registered as a result of:

- reorganization or liquidation legal entities;

- transfers, including acquisition, of property between persons recognized as interdependent in accordance with paragraph 2 of Article 105.1 of the Tax Code of the Russian Federation.

These exceptions do not apply to railway rolling stock manufactured from January 1, 2013 (the date of production is determined on the basis of technical passports).

Note! The terms of payment of advance payments and tax on movable property are set by the subjects of the Russian Federation. Therefore, dates may vary from region to region.

1. Organizations on DOS(including separate subdivisions with a separate balance sheet), which have fixed assets on their balance sheet that are recognized as an object of taxation for property tax.

2. Organizations on the simplified tax system and UTII, owning .

3. Organizations on ESHN for some property.

Corporate property tax: real estate

This tax applies to all real estate, except land plots and other objects of nature management (clause 1, clause 1, clause 4, article 374 of the Tax Code of the Russian Federation).

Moreover, real estate taxation has its own peculiarities. So, organizations on DOS must pay property tax in relation to:

- real estate listed on the balance sheet as fixed assets;

- residential real estate, not taken into account according to the data accounting like OS.

Organizations on the simplified tax system and UTII pay tax (clause 1 of article 378.2 of the Tax Code of the Russian Federation) if they own:

- , for example, shopping centers or premises in them. Full list such real estate is given in paragraph 1 of Art. 378.2 of the Tax Code of the Russian Federation;

- residential real estate, which is not accounted for on the balance sheet according to accounting data as a fixed asset.

Organizations on the Unified Agricultural Tax pay tax on property that is not used in the production of agricultural products, primary and subsequent (industrial) processing and sale of these products, as well as in the provision of services by agricultural producers (clause 3 of article 346.1 of the Tax Code of the Russian Federation).

Corporate property tax: movable property

The tax on movable property has not been paid since 01/01/2019 (Federal Law of 08/03/2018 No. 302-FZ).

Corporate property tax: tax base

By general rule the tax base is the average annual value of the property, but in respect of the tax is calculated based on its cadastral value(Art. 375, 378.2 of the Tax Code of the Russian Federation).

Property tax of legal entities: reporting periods

Reporting periods for property tax depend on the tax base (clause 2, article 379 of the Tax Code of the Russian Federation):

By the way, regional authorities may not establish reporting periods(Clause 3, Article 379 of the Tax Code of the Russian Federation).

Tax period for property tax

Taxable period for the property tax of organizations is the same for all (regardless of the value of the property, on the basis of which the tax is calculated) and is equal to calendar year(Clause 1, Article 379 of the Tax Code of the Russian Federation).

Corporate property tax rate

Regional authorities have the right to set the property tax rate themselves, but its amount cannot exceed the rate established by the Tax Code (clause 1, article 380 of the Tax Code of the Russian Federation). This rate is generally 2.2%.

At the same time, it is allowed to establish differentiated tax rates depending on the categories of taxpayers or property recognized as an object of taxation (clause 2 of article 380 of the Tax Code of the Russian Federation).

If the regional authorities have not set their own corporate property tax rates, then the tax is calculated based on the rates specified in the Tax Code of the Russian Federation (clause 4, article 380 of the Tax Code of the Russian Federation).

Calculation of corporate property tax

The tax calculation based on the average annual value of the property differs from the tax calculation based on the cadastral value.

And here it is important to note that when calculating the tax based on the average annual value, it is not necessary to take into account real estate, the tax in respect of which is calculated based on the cadastral value.

Calculation of advance payments and tax based on the average annual value of the property

To calculate the advance, you need to determine average cost property (clause 4, article 376 of the Tax Code of the Russian Federation):

Having determined the average value of the property, you can calculate the amount of the advance payment (clause 4 of article 382 of the Tax Code of the Russian Federation):

To calculate the annual tax amount, you need to determine the average annual value of the property:

The tax calculation looks like this:

At the end of the year, you need to pay extra to the budget by the amount calculated according to the formula:

Calculation of advance payments and tax based on the cadastral value of the property

To understand how much advance payment you need to pay to the budget, you need to make the following calculation (clause 12, article 378.2 of the Tax Code of the Russian Federation):

Annual amount tax is determined by following formula:

And the amount of tax payable at the end of the year is calculated as follows:

Deadline for paying corporate property tax

The deadline for paying property tax is established by the laws of the constituent entities of the Russian Federation (clause 1, article 383 of the Tax Code of the Russian Federation).

For example, owners of Moscow property must pay tax at the end of the year no later than March 30 of the year following the reporting year (clause 1, article 3 of the Law of the City of Moscow dated 05.11.2003 N 64). And the deadline for payment for payers of property tax in the Republic of Tatarstan is April 5 of the year following the reporting year (part 3, article 4 of the Law of the Republic of Tajikistan dated November 28, 2003 No. 49-ZRT).

Deadline for payment of advance property tax payments

The deadlines for the payment of advance payments, as well as the deadline for paying taxes, are set by the regional authorities. And, accordingly, in different regions, these terms may be different.

Submission of reporting on corporate property tax

Payers of property tax must submit reports on this tax in the following terms:

| Type of reporting | When it appears | Submission deadline |

|---|---|---|

| Calculation of the advance payment for property tax (Appendix No. 4 to the Order of the Federal Tax Service of March 31, 2017 No. ММВ-7-21 / [email protected]) | According to the results of the reporting periods | Not later than the 30th day of the month following the reporting period (clause 2, article 386 of the Tax Code of the Russian Federation) |

| Declaration (Appendix No. 1 to the Order of the Federal Tax Service of March 31, 2017 No. ММВ-7-21/ [email protected]) | At the end of the year | Not later than March 30 of the year following the reporting year (clause 3 of article 386 of the Tax Code of the Russian Federation) |

If reporting periods are not established in your region, then, accordingly, you only need to submit a declaration at the end of the year to the Federal Tax Service Inspectorate.

It is not necessary to submit a calculation and a declaration if the organization does not have taxable property.

The nuances of payment and reporting

Organizations must pay advances/tax at the location of the property:

| Property location | Where is the tax paid? |

|---|---|

| The property is located at the location of the organization (clauses 3, 6 of article 383 of the Tax Code of the Russian Federation) | In the IFTS, where the organization is registered |

| The property is located separate subdivision having a separate balance sheet (Article 384 of the Tax Code of the Russian Federation) | In the IFTS, where the EP is registered |

| Real estate is located outside the location of the organization and the EP (Article 385 of the Tax Code of the Russian Federation) | In the IFTS serving the territory where the property is located |

The same procedure applies to reporting on property tax (clause 1, article 386 of the Tax Code of the Russian Federation).

If the organization owned the property for less than a year

If taxable property was registered not from the beginning of the reporting year or retired during the year, then this fact will not affect the formula for calculating advances/tax based on the average annual value of the property.

If we are talking about property, the tax in respect of which is calculated based on the cadastral value, then advances / tax are calculated taking into account the ownership ratio (clause 5, article 382 of the Tax Code of the Russian Federation). This coefficient is determined by the following formula:

When calculating the number of full months of ownership, you need to consider that:

- if the ownership of cadastral real estate arose before the 15th day of a particular month inclusive, then this month is taken as a full month. If the right to real estate arose after the 15th day of the month, then this month is not taken into account;

- if the ownership of cadastral real estate is terminated after the 15th day of the month, then this month is included in the calculation of the coefficient as a full month. If the right is terminated before the 15th day of the month inclusive, then such a month does not need to be taken into account.

In our article you can read how to do it right posting property tax in accounting and how to file a property tax return.

Property subject to property tax includes buildings, structures. That is, those objects that cannot be moved without prejudice to their purpose. At the same time, it is not necessary to pay or objects of construction in progress, although they are also classified as real estate. The explanation here is simple. Land plots are subject to a separate tax. And objects of construction in progress are not fixed assets, which means that they are not taken into account when calculating property tax.

Recognized as movable property objects that do not fall under the definition of real estate.

This follows from the provisions of subparagraph "a" of paragraph 4 and paragraph 5 of PBU 6/01, Article 130 Civil Code RF, articles 374 tax code of the Russian Federation and is confirmed by letters of the Ministry of Finance of Russia dated February 25, 2013 No. 03-05-05-01 / 5322 and the Federal Tax Service of Russia dated February 18, 2013 No. BS-4-11 / 2677.

When determining the composition of property, be also guided by the Law of December 30, 2009 No. 384-FZ and All-Russian classifier fixed assets (OKOF), approved by the Decree of the State Standard of Russia dated December 26, 1994 No. 359. Such explanations are also in the letter of the Ministry of Finance of Russia dated February 25, 2013 No. 03-05-05-01 / 5322.

Residential buildings and residential premises are recognized as objects of property taxation, regardless of which group of assets they are assigned to in accounting. Residential properties accounted for as fixed assets are taxed on the basis of paragraph 1 of Article 374 of the Tax Code of the Russian Federation. BUT residential buildings, not included in fixed assets - on the basis of Article 378.2 of the Tax Code of the Russian Federation.

For example, if an organization purchased a dwelling for resale, then in accounting it can be reflected on account 41 “Goods”. Despite the fact that this is not a fixed asset, since 2015 such premises may also be subject to property tax (subclause 4, clause 1, article 378.2 of the Tax Code of the Russian Federation). But since the tax base for such residential buildings (premises) is cadastral value , in regional law on the property tax of organizations, they should be named as part of the objects of taxation. If there is no such provision in the regional law, it is not necessary to pay property tax for residential properties that are not included in fixed assets.

This follows from the provisions of paragraph 1 of article 374, paragraph 2 of paragraph 2 of article 372, paragraph 1 of article 378.2 of the Tax Code of the Russian Federation and letters of the Ministry of Finance of Russia dated May 28, 2015 No. 03-05-05-01 / 30895, dated May 6, 2015. No. 03-05-05-01/25946, March 30, 2015 No. 03-05-05-01/17315.

Thus, the following are subject to property taxation:

– fixed assets , accounting for which is regulated by the rules of PBU 6/01 and Guidelines, approved by order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n;

- residential buildings and residential premises, regardless of whether they are fixed assets or not.

From this rule, there are two exceptions.

Firstly, you do not need to pay tax on fixed assets that are recognized as movable or immovable property, but which are excluded from the list of objects of taxation by paragraph 4 of Article 374 of the Tax Code of the Russian Federation.

These fixed assets include:

- land, water bodies and Natural resources;

- fixed assets of power structures;

- objects cultural heritage;

- nuclear installations that are used for scientific purposes, as well as storage facilities for nuclear materials, radioactive substances and waste;

- icebreakers, nuclear-powered ships and nuclear-technological service vessels;

- space objects;

- ships registered in the Russian International Ship Register;

- any fixed assets included in the first or second depreciation group according to the Classification approved by the Decree of the Government of the Russian Federation of January 1, 2002 No. 1.

And secondly, there is no need to pay tax on fixed assets that are recognized as objects of taxation, but for which benefits apply provided for by Article 381 of the Tax Code of the Russian Federation.

Important: along with benefits of a sectoral or social nature, Article 381 of the Tax Code of the Russian Federation establishes a benefit that can be used by any organization that has movable property on its balance sheet. It's about on exemption from taxation of movable property registered on January 1, 2013 and later. This benefit cannot be applied to movable property that was registered as a result of:

- reorganization (liquidation) of the organization;

- transactions between related parties.

This procedure is established by paragraph 25 of Article 381 of the Tax Code of the Russian Federation.

It should be noted that changes that organizations make to their names or constituent documents in connection with the new requirements of Chapter 4 of the Civil Code of the Russian Federation are not recognized as reorganization. For example, if a CJSC becomes non-public joint stock company(Article 66.3 of the Civil Code of the Russian Federation). In such cases, the exemption for movable property registered after December 31, 2012 remains. If a change in name (correction of constituent documents) entails a change in the organizational and legal form (for example, a CJSC is transformed into an LLC), the successor organization loses the right to the benefit.

Such clarifications are contained in the letters of the Ministry of Finance of Russia dated February 9, 2015 No. 03-05-05-01 / 5111 and the Federal Tax Service of Russia dated January 20, 2015 No. BS-4-11 / 503.

If the property registered after December 31, 2012, the organization acquired through an intermediary, it can also take advantage of the benefits provided for in paragraph 25 of Article 381 of the Tax Code of the Russian Federation. But only on condition that the seller of the property is not an interdependent person either in relation to the intermediary, or in relation to the customer organization itself. This is stated in the letter of the Ministry of Finance of Russia dated March 30, 2015 No. 03-05-05-01 / 17304.

The following table will help determine the composition of movable property from which tax must be paid in 2016:

|

Grounds for registering property |

Depreciation groups, which include an object of movable property, according to the Classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1 |

|

|

First or second |

Other |

|

|

The receipt of property as a result of the reorganization or liquidation of the legal predecessor organization |

||

|

Receipt of property as a result of a transaction with a related person |

Not taxed (subclause 8, clause 4, article 374 of the Tax Code of the Russian Federation) |

Subject to (clause 25, article 381 of the Tax Code of the Russian Federation) |

|

Other grounds |

Not taxed (subclause 8, clause 4, article 374 of the Tax Code of the Russian Federation) |

Subject to (Article 374 of the Tax Code of the Russian Federation) |

|

The receipt of property as a result of the reorganization or liquidation of the legal predecessor organization. At the same time, reorganization means, among other things, a change in the organizational and legal form of the organization. For example, when a CJSC becomes an LLC (letters of the Ministry of Finance of Russia dated January 16, 2015 No. 03-05-05-01 / 676 and the Federal Tax Service of Russia dated January 20, 2015 No. BS-4-11 / 503). |

Not taxed (subclause 8, clause 4, article 374 of the Tax Code of the Russian Federation) |

Subject to (clause 25, article 381 of the Tax Code of the Russian Federation) |

|

The receipt of property as a result of a transaction with related person (Letters of the Ministry of Finance of Russia dated January 16, 2015 No. 03-05-05-01/676 and the Federal Tax Service of Russia dated January 20, 2015 No. BS-4-11/503) |

Not taxed (subclause 8, clause 4, article 374 of the Tax Code of the Russian Federation) |

Subject to (clause 25, article 381 of the Tax Code of the Russian Federation) |

|

Other grounds |

Not taxed (subclause 8, clause 4, article 374 of the Tax Code of the Russian Federation) |

Not taxed (clause 25, article 381 of the Tax Code of the Russian Federation) |

Fixed assets included in the first or second depreciation group are not subject to property tax, regardless of the date they were registered (letter of the Ministry of Finance of Russia dated April 7, 2015 No. 03-05-05-01 / 19338).

Situation: whether it is necessary to pay property tax on movable property received by the organization as a contribution to authorized capital?

Yes, it is necessary if the parties to the transaction are interdependent persons, and the movable property belongs to the third to tenth depreciation groups.

Fixed assets included in the first or second depreciation group according to the Classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1 are not recognized as an object of taxation in principle. Therefore, if the organization received such property in the authorized capital, it is not necessary to pay tax on it.

If movable property is assigned to other depreciation groups, the organization also has the opportunity not to pay tax. The fact is that movable property registered on January 1, 2013 falls under the exemption provided for by paragraph 25 of Article 381 of the Tax Code of the Russian Federation. However, this exemption is subject to restrictions, one of which is the acquisition of property from related person .

Is the transfer of property recognized as a contribution to the authorized capital as a transaction with a related person? Yes, it is recognized if the share of participation of the person who made the contribution exceeds the amount established by paragraph 2 of Article 105.1 of the Tax Code of the Russian Federation (as a rule, 25%).

Does the time gap between the date of transfer of property and the date of registration of an increase in the authorized capital affect the taxation of property? No, it doesn't. The presence of interdependence between the parties confirms the very decision to participate in the authorized capital with a share exceeding 25 percent. The transfer of property indicates that the transaction took place. And making changes to the constituent documents and registering these changes in the Unified State Register of Legal Entities is just a formality that certifies the rights of the founder (participant, shareholder).

Thus, if as a result of a transaction for the transfer of movable property to the authorized capital, the organization and the founder (participant, shareholder) become interdependent persons, the received fixed assets must be included in the calculation of the tax base for property tax. Provided that these assets belong to the third to tenth depreciation groups. tax base must be increased from the moment the property is actually transferred to the deposit.

If, as a result of the transaction, the organization and the founder (participant, shareholder) do not become interdependent persons, movable property received as a contribution to the authorized capital is exempt from taxation.

This follows from the provisions of subparagraph 8 of paragraph 4 of article 374, paragraph 25 of article 381 of the Tax Code of the Russian Federation and letters of the Ministry of Finance of Russia dated January 16, 2015 No. 03-05-05-01 / 676 and the Federal Tax Service of Russia dated January 20, 2015 No. BS- 4-11/503.

Situation: whether it is necessary to pay property tax on movable property received by a unitary enterprise for economic management (as a contribution to the statutory fund) from the administration municipality ?

No, it doesn `t need.

The fact is that fixed assets of the first or second depreciation group according to the Classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1 are not taxed in principle. And for movable property from other depreciation groups unitary enterprise has the right to use the privilege established by paragraph 25 of Article 381 of the Tax Code of the Russian Federation. That means you don't have to pay taxes.

At the same time, the exception provided for by this article for related parties (that is, when the benefit does not apply) does not apply to the enterprise and administration. After all, the interdependence between them is not defined, since only organizations or organizations can be interdependent persons. individuals. And the administration of the municipality does not belong to these categories (clause 5, article 105.1 of the Tax Code of the Russian Federation).

This follows from the provisions of subparagraph 8 of paragraph 4 of article 374, paragraph 25 of article 381 of the Tax Code of the Russian Federation and letters of the Ministry of Finance of Russia dated February 6, 2015 No. 03-05-05-01 / 5030, dated January 16, 2015 No. 03-05- 05-01/676 and the Federal Tax Service of Russia dated January 20, 2015 No. BS-4-11/503.

Situation: Is it necessary to pay property tax for a movable fixed asset installed by an interdependent organization? Mounting equipment purchased after January 1, 2013 from a seller who is not related.

No, it doesn `t need.

If movable property accounted for as property, plant and equipment is made from materials purchased after January 1, 2013, then such property does not need to be taxed. At the same time, it does not matter whether the organization - the owner of the fixed asset is interdependent in relation to:

- to the seller of equipment and materials from which the fixed asset was assembled;

- to the organization that was engaged in the assembly (installation) of equipment.

In this case, the rule applies that movable property registered as fixed assets from January 1, 2013 is exempt from taxation. Yes, there is an exception. A movable object that was purchased from an interdependent person is taxed regardless of the date of registration (clause 25, article 381 of the Tax Code of the Russian Federation).

However, the situation under consideration does not fall under such an exception. After all, the organization did not acquire a fixed asset from an interdependent person. The related person (contractor) only completed the installation of the fixed asset from the materials provided to him. And the materials themselves are not subject to property tax. And interdependence with the contractor does not limit the right of the organization to apply the benefits provided for in paragraph 25 of Article 381 of the Tax Code of the Russian Federation.

Thus, the fixed asset, assembled by an interdependent contractor, is exempt from taxation at the customer. A similar conclusion can be drawn from the letters of the Ministry of Finance of Russia dated March 5, 2015 No. 03-05-04-01 / 11797 (brought to the attention of tax inspections letter of the Federal Tax Service of Russia dated March 13, 2015 No. ZN-4-11/4037), dated March 30, 2015 No. 03-05-05-01/17289.

Situation: Is it necessary to pay property tax for a movable fixed asset assembled by an interdependent organization from its own materials? The fixed asset was accepted for balance after January 1, 2013.

Yes need. Let's explain why.

As a general rule, movable property registered as fixed assets from January 1, 2013 is exempt from taxation. But there is an exception. A movable object that was purchased from an interdependent person is taxed regardless of the date of registration (clause 25, article 381 of the Tax Code of the Russian Federation).

Method and documenting the acquisition of property for the application of the named benefits does not matter. The main thing is that the organization received the main means from an interdependent person. In practice, this transfer could be formalized by a sale and purchase agreement, a sale and purchase agreement with a condition for the installation of a fixed asset by the supplier, a contract for the manufacture of a fixed asset from the contractor’s materials, etc. In each of these cases, the party transferring the object to the organization is an interdependent with her counterparty: seller or contractor.

Therefore, for a movable fixed asset assembled by an interdependent organization from its own materials, the organization that received the object must pay property tax.

This follows from the provisions of paragraph 25 of Article 381 of the Tax Code of the Russian Federation.

Situation: Should a simplified organization pay property tax on parking spaces located in an administrative office building?

The answer to this question depends on two factors:

- whether the administrative and office building is included in the list of objects, the tax on which is paid based on the cadastral value;

- whether the organization is the owner of parking spaces (does it own them on the right of economic management).

Simplified organizations pay property tax only on real estate, the base for which is considered based on the cadastral value. The composition of such objects is determined by the regional authorities. You can see them in the lists that are published on the official websites of the constituent entities of the Russian Federation. If the building is included in the list, then a tax will have to be paid from the parking space. But only if it is owned by the organization. After all, only owners and organizations that own objects on the right of economic management should pay property tax based on the cadastral value of real estate. This is established by paragraph 2 of article 346.11, paragraph 7 and subparagraph 3 of paragraph 12 of article 378.2 of the Tax Code of the Russian Federation.

And what is the cost of paying tax? After all, a parking space is only part of the building.

Indeed, parking spaces themselves are not separate premises. In particular, in office buildings they are usually located in underground parking lots without any partitions. Nevertheless, you still need to pay tax on a parking space. It is integral part underground parking, which, in turn, is part of the building as a separate and specially equipped room (clause 5.2.1 of the Code of Rules approved by order of the Ministry of Regional Development of Russia dated December 29, 2011 No. 635/9). Therefore, the ownership of parking spaces is registered on a shared basis. That is, not the whole object is transferred to the ownership of the organization, but a share in it, corresponding to the area of parking spaces. In accounting, such objects are reflected in the composition of fixed assets at their original cost, proportional to the share in common ownership.

Thus, with next month after the inclusion of parking spaces in the composition of fixed assets, they become the object of taxation. Calculate the property tax for such objects based on the share of the cadastral value proportional to the size of parking spaces in total area building or parking space. This follows from the provisions of paragraph 6 of Article 378.2 of the Tax Code of the Russian Federation and is confirmed by the letters of the Federal Tax Service of Russia dated April 23, 2015 No. BS-4-11 / 7028, dated April 27, 2015 No. GD-4-3 / 7143.

Attention: in Moscow, organizations that own multi-story parking garages are exempt from paying property tax on these facilities. However, in this situation, this exemption does not apply.

Since 2016, the benefit applies only to multi-storey parking garages located in separate buildings. If the parking lot is located in an administrative and office complex or in mall, it is subject to property tax at the cadastral value on a general basis. This procedure is provided for by subparagraph 9 of paragraph 1 of Article 4 of the Law of the City of Moscow dated November 5, 2003 No. 64.

Situation: Do I need to pay property tax on movable property acquired before January 1, 2013? Organization - the owner of the property is located in the Crimea (Sevastopol).

Yes need.

Movable property accounted for as fixed assets before January 1, 2013 is recognized as an object of property taxation. The only exception is if the property is included in the first or second depreciation group according to the Classification approved by Decree of the Government of the Russian Federation of January 1, 2002 No. 1.

Prior to the annexation of the territories of Crimea and Sevastopol to Russia, the dates of acceptance of property for accounting by organizations located in these regions were determined according to Ukrainian legislation. After entering data on these organizations into the Russian Unified State Register of Legal Entities, neither the date of registration of the property nor the value of the property are reviewed. This follows from the provisions of paragraph 5.1 of the information of the Ministry of Finance of Russia dated July 11, 2014 No. PZ-12/2014. Thus, in order to calculate the property tax on Russian legislation the dates of acceptance for accounting of property acquired before January 1, 2013 remain the same.

Under Russian law, movable property registered as fixed assets from January 1, 2013 is exempt from taxation. An exception to this rule is made only in relation to movable property, which was transferred to the organization as a result of the reorganization (liquidation) of the legal predecessor or was acquired from an interdependent person. Such assets are subject to property tax regardless of the date of registration (clause 25, article 381 of the Tax Code of the Russian Federation).

The entry of data on the organization into the Unified State Register of Legal Entities is not recognized as a reorganization (clause 6, article 19 of the Law of November 30, 1994 No. 52-FZ). Therefore, in the situation under consideration, the re-registration of an organization under Russian law does not affect the taxation of its movable property in any way. The date of entering information about the organization in the Unified State Register of Legal Entities cannot be considered as the date of registration of property.

Given the above, from movable property acquired before January 1, 2013, an organization located in the Crimea (Sevastopol) and registered in the Russian Unified State Register of Legal Entities must pay property tax on a general basis.

Movable property, which, according to Ukrainian legislation, was registered from January 1, 2013, is exempt from taxation. The exemption provided for by paragraph 25 of Article 381 of the Tax Code of the Russian Federation in the event of reorganization (liquidation) also applies regardless of the date the information about the organization was entered into the Russian Unified State Register of Legal Entities.

Since 2018, the rules for calculating property tax on movable fixed assets registered since January 01, 2013 have changed. This article will tell you what the essence of these innovations are and what explanations were given by officials.

You will also learn:

- where and how to specify the tax rate in 1C for movable property;

- how to find out if the "movable" benefit is preserved in your region;

- at what rate to calculate the tax if the benefit is no longer valid;

- how to reflect in the benefits in 1C and in tax reporting.

Tax rates on movable property

From January 01, 2018, the federal benefit established by paragraph 25 of Art. 381 of the Tax Code of the Russian Federation, which exempted movable property registered from 01/01/2013 from tax, has been canceled. However, it can be preserved, but only if the relevant law is adopted by the constituent entities of the Russian Federation (clause 1, article 381.1 of the Tax Code of the Russian Federation).

In those constituent entities of the Russian Federation, whose laws do not provide for a privilege on movable property and the rate is not indicated, it is necessary to pay a tax at a rate of 1.1% (Letter of the Federal Tax Service of the Russian Federation of December 20, 2017 N BS-19-21 / 327). Whether benefits or reduced rates are provided for your region, you can check on the official website of the tax service

Letter dated March 28, 2018 N BS-4-21/ [email protected] The Federal Tax Service of the Russian Federation brought to its subdivisions the Letter of the Ministry of Industry and Trade of the Russian Federation dated March 23, 2018 N OV-17590-12, which clarifies the issue of classifying fixed assets as movable and immovable property.

Machinery and equipment named in OKOF in section 330.00.00.00.000 “Other machines and equipment, including household inventory and other objects, located both in the building and outside it, even if attached to the building on the foundation, are considered movable property, as they perform independent production functions.

From 2018, the following rates for property taxation are applied to movable property registered from 01/01/2013:

- the maximum rate of 1.1% - if the regional law does not establish benefits, lower rates, or the maximum rate is set;

- reduced rate, in accordance with the amount established by regional law;

- reduced rate or benefit for individual objects, according to regional laws;

- exemption from property tax, i.e. exemption has been preserved by regional law.

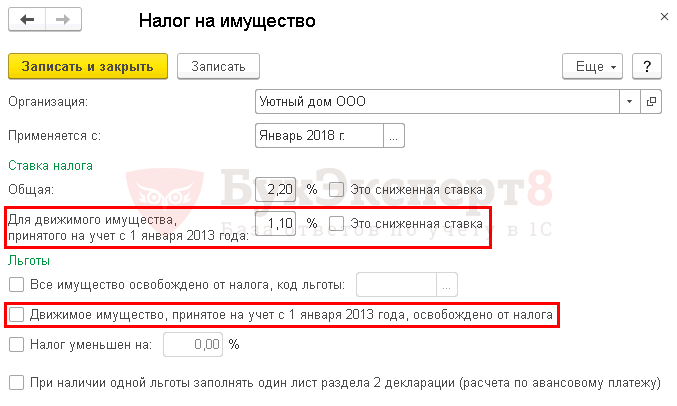

Property tax rates in 1C

Property tax rates for an organization are indicated in the section Directories - Taxes - Property tax - link Rates and benefits.

The program automatically sets after updating to release 3.0.57 new rate property tax for movable property, which has been in force since 2018 and is established at the federal level (clause 3.3 of article 380 of the Tax Code of the Russian Federation). If a different rate is set by the region, then it must be set manually in the information register Property tax.

If it is necessary to set a different rate or benefit for individual property objects, then for these fixed assets it is necessary to set the settings in information register Property tax: Objects with a special taxation procedure In chapter Directories - Taxes - Property tax - link Objects with a special taxation procedure.

Benefit (rate) code in the property tax return

If the local law provides for a benefit or reduced rate for property tax, then, depending on the article of the Tax Code of the Russian Federation, on the basis of which the benefit or rate is provided, a code is determined (Appendix No. 6 "Tax benefit codes" to the Procedure for filling out tax return and advance payment for corporate property tax, approved. Order of the Federal Tax Service of the Russian Federation dated March 31, 2017 N MMV-7-21 / [email protected]).

The correct setting in 1C of rates and benefits for property tax will ensure the correct automatic filling of the declaration and advance payments. For each benefit code, a separate sheet of Section 2 is completed.

If the region provides benefits with codes:

- 2012000 "tax incentives for tax established by the laws of the constituent entities of the Russian Federation, except for tax incentives in the form of a reduction in the rate and in the form of a reduction in the amount of tax";

- 2012400 "tax benefits for tax ... in the form of a reduction in the tax rate for separate category taxpayers";

- 2012500 "tax benefits for tax ... in the form of a reduction in the amount of tax payable to the budget",

then in the declaration after such codes, through a slash, you must manually indicate the data of the law of the subject of the Russian Federation, which established the benefit (Letter of the Federal Tax Service of the Russian Federation of March 14, 2018 N BS-4-21 / [email protected]).

This must be done in the format:

- article,

- paragraph,

- subparagraph

4 characters are allocated for each value. Unused characters are indicated by zeros.

Consider in detail the options for taxing movable property.

Benefit saved

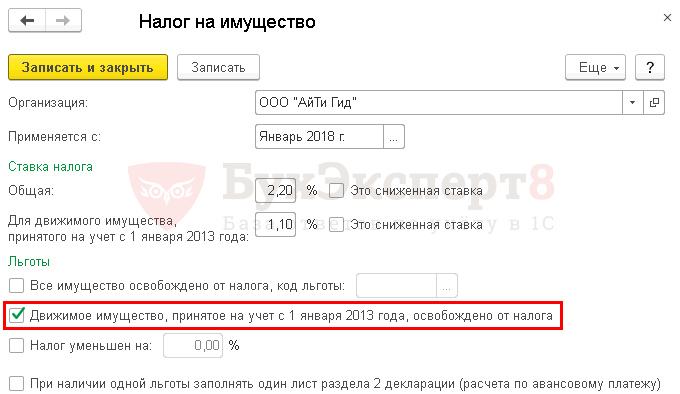

Let us analyze the features of calculating the tax on movable property while maintaining benefits using the example of Moscow.

In the information register Property tax necessary:

- check the box Movable property registered on January 1, 2013 is exempt from tax .

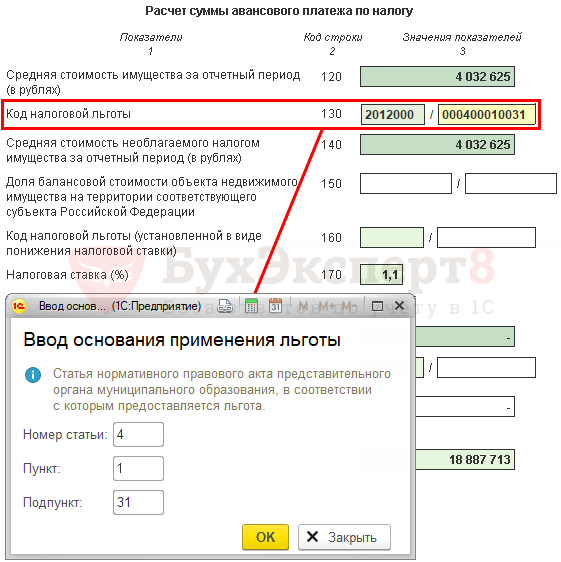

In the declaration (calculation of advance payments) for property tax in pages 160 (130) of Section 2, the code of the benefit and the law under which it is granted are manually indicated:

- instead of a benefit code 2010257 the code is indicated 2012000 “Additional property tax benefits established by the laws of the constituent entities of the Russian Federation ...”;

- fill in the data of the law of the subject of the Russian Federation 000400010031 . In our example, the benefit is granted on the basis of paragraphs. 31 p. 1 art. 4 Law of the city of Moscow dated 05.11.2003 N 64.

Benefit retained partially

And now let's consider the features of calculating the tax on movable property, if the exemption is retained only for a certain number of movable property, using the example of St. Petersburg.

In the information register Property tax nothing needs to be changed:

- — 1,1

- checkbox This is a reduced rate. not installed.

In order to determine if it falls under this benefit movable property, it is necessary to determine its age, i.e. the number of years that have passed since the year the property was issued.

In 1C, for property objects for which a benefit is established, it is necessary to fill in information in the form Property tax: an object with a special taxation procedure.

- tax credit — Exempted from taxation, the exemption applies, because the date of issue of the car is 08.10.2016 and from this date no more than 3 years have passed; PDF

- The code tax break — 2012000 .

Declaration (calculation of advance payments) for property tax

In the declaration (calculation of advance payments) for property tax in pages 160 (130) of Section 2, the code of the benefit and the law under which it is granted are indicated:

- automatically fill in the benefit code 2012000 "Additional property tax benefits established by the laws of the constituent entities of the Russian Federation ...".

- manually fill in the data of the law of the subject of the Russian Federation 04-100010024 . In our example, the benefit is granted on the basis of Art. 4-1 p. 1 p. 24 Law of the city of St. Petersburg dated November 26, 2003 N 684-96.

Reduced rate, incl. 0%

The amount of the tax rate is established by federal or regional law. Be sure to clarify in the law of your region how the authorities approved the benefit - this is very important for filling out the report.

The subject of the Russian Federation can establish:

- reduced tax rate, incl. 0%;

- reduced rate benefit.

If a reduced or zero rate is mentioned in the regional law in the “Rates” section, the benefit code is not affixed!

Consider the features of calculating the tax on movable property if a reduced tax rate is used, using the example of the Moscow Region, which simply has a reduced rate and Tyumen region, in which the reduced rate is set as a benefit.

Reduced rate

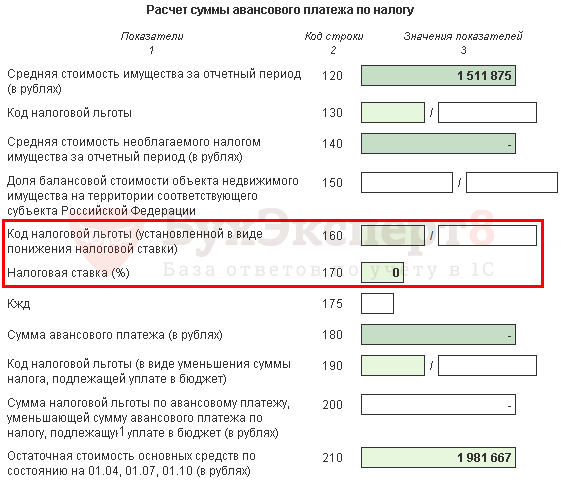

In the information register Property tax necessary:

- For movable property registered from January 1, 2013 - install 0% ;

- checkbox This is a reduced rate. do not install, because the reduced rate is not set as a benefit.

Declaration (calculation of advance payments) for property tax

- p. 210 (170) "Tax rate (%)" - 0.

Reduced rate as a benefit

In the information register Property tax necessary:

- For movable property registered from January 1, 2013 - install 0,55% ;

- checkbox This is a reduced ratea installed, because in the Tyumen region, a privilege in the form of a reduced rate has been established.

Declaration (calculation of advance payments) for property tax

In the declaration (calculation of advance payments) for property tax, on page 200 (160) of Section 2, the code of the benefit established in the form of a reduction in the tax rate and the law under which it is granted are indicated:

- automatically fill in the benefit code 2012400 “Tax incentives for tax established by the laws of the subjects Russian Federation in the form of a reduction in the tax rate for a certain category of taxpayers.

- manually fill in the data of the law of the subject of the Russian Federation 0004 0000 0000 . In our example, the reduced rate is set on the basis of Art. 4 Law of the Tyumen region dated October 24, 2017 N 74.

Benefit not saved, rate 1.1%

Consider the features of the calculation of the tax on movable property, if the benefit is not saved, using the example of the Samara region.

In the information register Property tax nothing needs to be changed:

- For movable property registered from January 1, 2013 — 1,1 %, i.e. default value;

- checkbox This is a reduced rate. not installed.

Declaration (calculation of advance payments) for property tax

Section 2 of the declaration (calculation of advance payments) for property tax will be completed in the usual way:

- p. 160 (130) "Tax benefit code" - not filled out;

- line 200 (160) “Tax benefit code (established in the form of a reduction in the tax rate)” - not filled out;

- p. 210 (170) "Tax rate (%)" - 1.1;

- p. 220 (180) "Tax amount (advance payment amount)" - the amount of the calculated tax (advance payment).