When choosing a bank for conclusion deposit agreement a potential depositor has to compare several parameters: interest rate, placement period, frequency of interest payments, the possibility of additional investment, conditions for early termination of the contract. The client also often hears from a banking specialist the concept of " capitalization of the deposit" and " interest capitalization". What is it and what benefits does the client receive from such deposits?

Capitalization of the deposit

Capitalization of the deposit is an increase in the original amount by the amount of accrued interest. At the same time, in the next period, interest is accrued on the initially invested funds. Upon expiration of the agreement, the bank will simply transfer the principal amount and accrued interest to the current or card account.

The agreement may also provide for automatic extension of the deposit with capitalization. This means that if the depositor does not apply to the bank on the day the contract ends, it will automatically be extended for the same period, and interest will be added to the investment amount.

implies the addition of accrued, according to the agreement, interest to the principal amount of the deposit. The accrual of interest for the next period is already carried out on the increased deposit amount. Thus, the compound interest formula is used, which allows the depositor to receive additional income.

implies the addition of accrued, according to the agreement, interest to the principal amount of the deposit. The accrual of interest for the next period is already carried out on the increased deposit amount. Thus, the compound interest formula is used, which allows the depositor to receive additional income.

The contract must specify the frequency of capitalization, namely:

- annual capitalization. This option is rarely used, only for long-term deposits.

- Quarterly capitalization. Interest is accrued and added to the initial deposit amount 3 months, quarter or year after the opening of the contract. Such capitalization will bring the investor more high income than the first option.

- Monthly capitalization - interest is added to the principal amount of the deposit at the end of each month. This scheme is the most common among banks and is in good demand among depositors.

- The highest income comes from daily capitalization, but it is not used by Russian banks.

The general formula for calculating capitalization income is as follows:

K \u003d S * (1 + r / m) m * n, where

K - the total amount that the client will receive at the end of the contract;

S - initial investment amount;

r - annual interest rate;

m - the number of accrual periods, that is, with a semi-annual capitalization m=2, with a monthly capitalization m=12.

n is the number of years.

For example, a depositor wants to put money in the bank in the amount of 100,000 rubles for 1 year at 10% per annum. If the terms of the contract do not provide for the capitalization of interest, then at the end of the term he will receive:

100,000 + 100,000 * 0.1 \u003d 110,000 rubles.

If the borrower collects interest and places the money again within two years, then in three years his income will be:

10,000*3 = 30,000 rubles

With quarterly capitalization the calculation of profit for three years will look like this:

100 000*(1+0,1/2) 4*3 = 134 488,88

Thus, the client will receive an income in the amount of 34,488.88 rubles

With monthly capitalization, the calculation is done as follows:

100 000*(1+0,1/12) 12*3 = 134 818,2

The net income of the investor will be 34,818.2

Thus, from the example it is clear that the more often capitalization is done, the higher the income of the investor will be.

To quickly calculate the profit from bank deposit you can use our online calculator return on investment.

How to choose a deposit?

Interest rates on deposits with and without capitalization differ. To compare the profitability of a particular bank offer, you need to compare the effective rate.

For example, if you mark up 100,000 at 10% for a year, but with monthly capitalization, then the income will be:

100000*(1+0,1/12) 12*1 = 110 471,3

To get the same return, but without interest capitalization, the annual interest rate should be:

110471.3/100000 = 1.105 or 10.5% per annum.

Deposits with interest capitalization are of interest to investors whose main goal is to maximize income. But the profitability of the deposit should be evaluated in terms of the effective rate. Banks very often use deposits with capitalization for marketing purposes, and in fact ordinary deposits bring great benefits to the depositor.

It is worth paying attention to deposits with capitalization when placement is planned Money on the long term(several years) without an annual appeal to the bank to renew the contract. Thus, the required amount is often accumulated by a certain date.

When is it not beneficial?

Capitalization is interesting, first of all, with a long-term placement of funds. Regular accrual will be more convenient in the following cases:

- The client wants to receive interest on a monthly basis, considering it as a regular additional income.

- For the client, the possibility of early termination of the contract is important or partial withdrawal. Such banking programs usually do not involve capitalization.

An additional significant advantage of interest capitalization is that once they are added to the principal amount, they are subject to the deposit insurance system. The main condition is that capitalization must be carried out before the date of occurrence insured event. Interest that was accrued, but not capitalized and not paid to the depositor, may be lost in the event financial problems jar.

It is not necessary for a modern adult to tell what a bank account is and what interest is charged on it. What's more - many of us ourselves are excellent at contributing with a simple calculator. However, simple arithmetic often fails before. Although capitalization is often determined to calculate compound interest, a calculator and a piece of paper are also enough. However, understanding the benefits of capitalization is hindered by our propensity for simple solutions. But let's try to objectively understand the situation.

How is the capitalization of interest on a deposit account calculated?

Capitalization of interest - this is the addition to the interest calculated on the original principal amount of interest accrued in previous deposit periods. This system originated several centuries ago, earned popularity among experienced investors, and then began to be massively offered by banks. It allows the depositor's income to grow faster than using simple interest, which is calculated only on the principal amount.

- a deposit of 1,000 rubles accrued simple interest at a rate of 10% - at the end of the year, the depositor already owns 1,100 rubles;

- in the second year, at the same rate, his contribution will increase by another 100 rubles and will be equal to 1,200 rubles.

But if interest in the second year were accrued both on the principal amount and on interest for the first year, then at the end of the second year the depositor would already have:

- 1000 + 10% = 1100;

- 1100 + 10% = 1210.

The result is obvious - 1200 rubles against 1210.

The difference of 10 rubles is achieved without any efforts of the owner of the funds, only due to a different interest calculation system.

Benefit of capitalization of interest on the deposit

The benefits of capitalization can already be seen in the previous example, but in order to understand the scale of this benefit, let's calculate a deposit in the amount of 100 thousand rubles, respectively - with simple interest and with capitalization:

The difference of 12 thousand 889 rubles speaks for itself.

Furthermore! The rate at which income grows with compound interest depends on the frequency of capitalization; the higher the number of recalculation periods, the greater the total income. If interest is recalculated not once a year, but once a month, then the surplus income from capitalization will increase. With weekly or daily capitalization, it will grow even faster.

He will take the same amount of 100 thousand rubles at 10% per annum, and place it in a deposit with a monthly capitalization (for the sake of saving space, let's look at only the first 3 years):

Months, years | The amount of accrued interest, rub. | The total amount of the deposit, rub. |

January 2018 | ||

February 2018 | ||

April 2018 | ||

August 2018 | ||

September 2018 | ||

October 2018 | ||

November 2018 | ||

December 2018 | ||

January 2019 | ||

February 2019 | ||

April 2019 | ||

August 2019 | ||

September 2019 | ||

October 2019 | ||

November 2019 | ||

December 2019 | ||

January 2020 | ||

February 2020 | ||

April 2020 | ||

August 2020 | ||

September 2020 | ||

October 2020 | ||

November 2020 | ||

December 2020 |

The difference compared to the simple accrual of interest is 20 thousand 590 rubles, compared to the annual capitalization - 19 thousand 827 rubles.

It is hard to believe that changing the order of interest calculation can make such a difference, but each of the figures in the table can be manually recalculated.

What conclusions follow from this? Main two:

- Capitalization brings tangible additional income, especially with significant terms of deposit placement.

- Capitalization is the result of an accurate calculation, even small changes in the original figures change the result many times over.

The last point is worth paying attention to because we often “estimate in our mind” future result, and then refine it with calculations. But complex mathematical operations are not very suitable for quick, approximate conclusions.

The most important benefits of capitalization have already been demonstrated in the previous section. It offers a noticeable income without additional effort and investment. Capitalization is of great importance for long term investment and hardly noticeable with short-term deposits.

To this we can add the opinion of authorities: Albert Einstein spoke of compound interest as “the greatest mathematical discovery in the history of mankind”, and Rothschild considered it “the 8th wonder of the world”. The latter must have been modest, since he earned noticeably more on compound interest than someone before him on seven other miracles.

However, capitalization also has disadvantages and difficulties:

- A deposit with frequent capitalization and without restrictions is harder to find. The effect of capitalization may be a discovery for an ordinary depositor, but not for a bank. Credit institutions are not at all inclined to pay more than expected by clients, they would rather raise the simple interest rate, which will be a bright advertisement for the deposit, than offer compound interest, especially for long-term investments.

- A capitalized deposit is more difficult to withdraw. Here the effect is already psychological. The benefit from capitalization increases gradually. The longer the deposit is in the bank, the more it brings to the owner. Therefore, touching the principal amount of the deposit and even interest is becoming increasingly difficult.

The most profitable deposits with capitalization

To assess the real benefit from a deposit with capitalization, it is better to focus not on the annual interest rate, but on the interest accrual plan in real monetary units.

A capitalization deposit calculator can also be useful; these programs are often offered by the banks themselves and websites with financial topics.

Particularly profitable, ceteris paribus, will be the capitalization of interest.

It is important that all accrued interest and additionally deposited funds become the basis for calculating new interest as soon as possible. To capitalize as often as possible. Such proposals for credit market meet, sometimes banks promise even daily capitalization. If the offered benefit is not compensated by some restrictions and commissions, then the deposit deserves attention.

10:17 19.12.2019Banks have attracted and will continue to attract deposits. If you go to make a deposit, then usually banks offer 2 types of deposits, depending on what happens to the interest accrued on your money. The first type of deposits is a deposit without capitalization. In this case, the interest of each payment interval (monthly or quarterly) is paid to your deposit account.

The second option - interest on the deposit is added to the amount of the deposit and further accrual in the new period for the amount of the deposit + interest from previous period. In general, the second option is more profitable and the income from it will be higher. But there is one BUT. Typically, the rates on deposits with capitalization are lower than for deposits without capitalization. To choose the most profitable deposit, you need to calculate the effective interest rate on the deposit. In the case of a deposit without capitalization, the effective rate = the initial rate of the bank.

Formula and example of calculating a deposit without capitalization

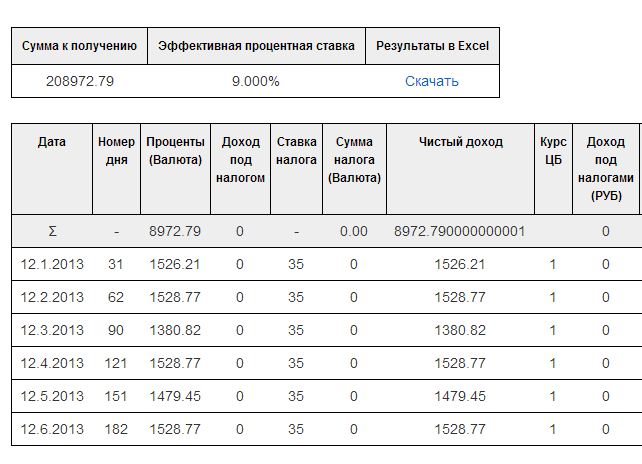

For an example of calculation, let's take the deposit of the KRK of the Kopilka bank

Under this offer of the bank, an interest rate of 9% per year is provided.

Let's say the amount of the initial deposit is 200 thousand rubles.

Term — 6 months or 182 days

The payment date is December 12, 2012.

The contribution provides monthly payment interest on the client's current account with the Bank, i.е. without capitalization.

We will try to receive payment on the deposit in January, February and March 2013.

To do this, consider the formula for calculating payments on a deposit without capitalization:

- Where Amount - the amount of funds deposited from the contract

- Interest rate - deposit rate

- The number of days in a year is 365 or 366, depending on whether it is a leap year or not.

- The number of days in the period is the difference between 2 next payment dates (well, or the date of the first payment and the payment date)

It should be noted that although the payment is made once a month, the bank calculates interest every day. As a result, monthly income depends on the number of days between 2 payment dates or on the actual number of days the money was in the bank.

The second nuance to consider is the interest rate per day. Since 2013 and 2012 have a different number of days, the formula should take into account the number of days in a year.

Thus, the interest formula for the period December 12, 2012 - January 12, 2013 will look like this:

By substituting our data into this formula, you can get the payment amount on January 12, 2013 from the CRC Bank.

Where S is the amount of the deposit payment that you will receive in your account. That is, for the first month, the income will be 1526.21 rubles.

Next, we calculate the payment for the period January 13, 2013 - February 12, 2013.

Here both dates are in the same year, you can use the first formula. You just need to calculate the difference between the dates

12.01.2013 — 12.02.2013 = 31

Substitute this difference and get the amount of interest in February

200 000 * 0.09*31/365 = 1528.77

And finally, we calculate the payment for February 13 - March 12, 2013 in the same way according to the formula.

We have a period of 28 days between February 12 - March 12

The return on your savings will be

200 000 * 0.09*28/365 = 1380.82

Similarly, you can calculate the income in subsequent months. Let's check our calculations with .

According to the payment schedule, it can be seen that the results obtained manually coincide with the results of the calculator. But not everything is so simple. The rate of 9 percent is quite a small rate. Consider the calculation of deposits with high rates.

Taxation if the deposit rate is higher than the Central Bank refinancing rate +5%

Now in all big banks deposit rates are low. There is no crisis and banks do not attract money. Another thing is the crisis, when banks offered deposit rates up to 20%.

It's pretty profitable proposition. But it should be noted that with a rate of 20% you will not receive 20% of the deposit amount at the end annual term. The fact is that income from a deposit at a rate higher than the refinancing rate of the Central Bank + 5% is subject to a 35 percent tax. This is only for ruble deposits

For foreign currency deposits- if the rate exceeds 9%, then you need to pay income tax. Those. the government takes its share of your savings income. At the same time, the effective interest rate decreases and it is no longer equal to the original one specified in the deposit agreement.

As of September 14, 2012, the Central Bank set the refinancing rate at 8.25% per annum.

Thus, we will determine the rate, from the interest on which a tax in the amount of 35% of income will be levied.

20 -(8.25 + 5) = 6.75%

Let's say % on our deposit is not 9%, but all 20%

Let's try to calculate the interest on the deposit for the first period.

It will be made up of income based on a rate of 20% minus 35 percent of income at a rate of 6.75%

Consider the calculation process

Moreover, the tax is rounded to whole numbers.

S1 - the amount of income before tax

S2 - the amount of tax withheld

Calculation for resident and non-resident.

It should also be taken into account that tax rate depends on whether you are a resident or not.

A non-resident is if you are a citizen of a state other than the Russian Federation.

For non-residents, the tax rate is 30%. For residents - 35 percent.

For example, let's calculate the first payment of our deposit at 20% for a non-resident.

The first payment in this case will be calculated according to the formulas

Those. S2 has changed because the rate of taxation on the deposit has changed. The accrued interest S1 remained the same.

The effective interest rate on such a deposit will be equal to 17.970% (Taken from the results of calculations of the deposit calculator)

It should be noted that these calculations can be easily implemented in Excel or you can use the above deposit calculator. He will be able to calculate the deposit without capitalization, and will also allow you to take into account deposits and withdrawals.

What is the capitalization of a deposit and the capitalization of interest on a deposit?

When choosing a bank to conclude a deposit agreement, a potential depositor has to compare several parameters: interest rate, placement period, frequency of interest payments, the possibility of additional investment, conditions for early termination of the agreement. The client also often hears from a banking specialist the concept of " capitalization of the deposit" and " interest capitalization". What is it and what benefits does the client receive from such deposits?

Capitalization of the deposit

Capitalization of the deposit is an increase in the original amount by the amount of accrued interest. At the same time, in the next period, interest is accrued on the initially invested funds. Upon expiration of the agreement, the bank will simply transfer the principal amount and accrued interest to the current or card account.

The agreement may also provide for automatic extension of the deposit with capitalization. This means that if the depositor does not apply to the bank on the day the contract ends, it will automatically be extended for the same period, and interest will be added to the investment amount.

It implies the addition of accrued, according to the agreement, interest to the principal amount of the deposit. The accrual of interest for the next period is already carried out on the increased deposit amount. Thus, the compound interest formula is used, which allows the depositor to receive additional income.

The contract must specify the frequency of capitalization, namely:

- annual capitalization. This option is rarely used, only for long-term deposits.

- Quarterly capitalization. Interest is accrued and added to the initial deposit amount 3 months, quarter or year after the opening of the contract. Such capitalization will bring the investor a higher income than the first option.

- Monthly capitalization - interest is added to the principal amount of the deposit at the end of each month. This scheme is the most common among banks and is in good demand among depositors.

- The highest income comes from daily capitalization, but it is not used by Russian banks.

The general formula for calculating capitalization income is as follows:

K=S*(1+r/m)m*n, where

K - the total amount that the client will receive at the end of the contract;

S is the initial investment amount;

r – annual interest rate;

m is the number of accrual periods, that is, with a semi-annual capitalization m=2, with a monthly capitalization m=12.

n is the number of years.

For example, a depositor wants to put money in the bank in the amount of 100,000 rubles for 1 year at 10% per annum. If the terms of the contract do not provide for the capitalization of interest, then at the end of the term he will receive:

100,000 + 100,000 * 0.1 \u003d 110,000 rubles.

If the borrower collects interest and places the money again within two years, then in three years his income will be:

10,000*3 = 30,000 rubles

With quarterly capitalization the calculation of profit for three years will look like this:

100 000*(1+0,1/2)4*3 = 134 488,88

Thus, the client will receive an income in the amount of 34,488.88 rubles

With monthly capitalization, the calculation is done as follows:

100 000*(1+0,1/12)12*3 = 134 818,2

The net income of the investor will be 34,818.2

Thus, from the example it is clear that the more often capitalization is done, the higher the income of the investor will be.

To quickly calculate the profit from a bank deposit, you can use our online deposit calculator.

How to choose a deposit?

Interest rates on deposits with and without capitalization differ. To compare the profitability of a particular bank offer, you need to compare the effective rate.

For example, if you allocate 100,000 at 10% for a year, but with a monthly capitalization, then the income will be:

100000*(1+0,1/12)12*1= 110 471,3

To get the same return, but without interest capitalization, the annual interest rate should be:

110471.3/100000 = 1.105 or 10.5% per annum.

Deposits with interest capitalization are of interest to investors whose main goal is to maximize income. But the profitability of the deposit should be evaluated in terms of the effective rate. Banks very often use deposits with capitalization for marketing purposes, and in fact ordinary deposits bring great benefits to the depositor.

It is worth paying attention to deposits with capitalization when it is planned to place funds for a long period (several years) without an annual appeal to the bank to renew the agreement. Thus, the required amount is often accumulated by a certain date.

When is it not beneficial?

Capitalization is interesting, first of all, with a long-term placement of funds. Regular accrual will be more convenient in the following cases:

- The client wants to receive interest on a monthly basis, considering it as a regular additional income.

- For the client, the possibility of early termination of the contract or partial withdrawal is important. Such banking programs usually do not involve capitalization.

An additional significant advantage of interest capitalization is that once they are added to the principal amount, they are subject to the deposit insurance system.

The main condition is that capitalization must be carried out before the date of the insured event.

Interest that was accrued, but not capitalized and not paid to the depositor, may be lost in case of financial problems of the bank.

Source: http://law03.ru/finance/article/kapitalizaciya-lada-chto-eto-takoe

Capitalization of the deposit - what is it?

Money should not lie idle ─ they should work and bring profit to their owner. This simple rule is known to many. When there are free financial resources a person faces the question of their reliable and profitable investment.

Most of our fellow citizens are not experts in investment and financial analytics.

Therefore, they prefer the simplest and most famous way - to open Bank deposit and earn interest on investments. Studying the numerous offers of different banks, they come across some unknown terms that determine the conditions for placing funds and the amount of income received.

With one of these terms, which is called capitalization, we will deal with this article.

What is the capitalization of interest on a deposit

Despite the rather unusual name, the essence of the concept of capitalization of interest on a deposit is quite simple: certain period(usually per month) interest is added to the principal amount of the deposit. In this case, the size of the deposit increases, and the next accrual of interest is already made on a larger amount.

Thus, income is brought not only by the initially placed funds, but also by all the interest accrued on them. This scheme is sometimes called compound interest deposit, because the final, or effective, rate on such a contribution is higher than the original one.

The most popular today are deposits with monthly, quarterly and annual interest capitalization. Deposits with daily and weekly capitalization rarely appear on the market. It is important to distinguish between the frequency of interest accrual and the frequency of capitalization of the deposit. For example, a bank can charge interest daily, and add monthly to the main body of the deposit.

Calculation of interest on a deposit with capitalization

In order to understand how the interest capitalization scheme works, consider a simple example. Let's say we have an amount of one hundred thousand rubles, and we want to place annual deposit at a rate of 10%.

Obviously, in the case of the usual accrual scheme (without capitalization), in a year the income on the deposit will be 0.1 * 100,000 = 10,000 rubles. Now let's try to calculate how much we can earn if we had a deposit with a monthly capitalization of interest and with the same rate.

- First month.

The accrued amount will be 100,000 * 31/365 * 0.1 = 849.32 rubles (here 365 is the number of days in a year, 31 is the number of days in a month, 0.1 or 10% is the deposit rate). By the end of the period, the deposit amount will be 100,849.32 rubles.

- Second month.

The interest on the deposit for this period is 100,849.32 * 30 / 365 * 0.1 = 828.90 rubles (we assumed that in the second month after opening the deposit, 30 calendar days, so the income turned out to be slightly less than in the first, but this is temporary, then everything will return to normal). Deposit amount RUB 101,678.22

- Third month.

The interest accrued by the bank will already be 101,678.22*31/365*0.1=863.57 rubles, and the placed amount will increase to 102,541.79 rubles.

- Fourth month. The calculated figures will be equal to 102,541.79 * 31/365 * 0.1 = 870.90 rubles and 103,412.69 rubles, respectively.

- Fifth-eleventh month.

All charges are made in the same way.

- Twelfth month. Accrued interest - 900.58 rubles, the amount of the deposit by the end of the term - 110,471.27 rubles.

As you can see, the interest capitalization formula is very simple, you only need to take into account all the intervals in the calculation.

So, having placed 100,000 rubles for one year at 10% with capitalization, we received 10,471.27 rubles of net income.

This corresponds to an effective rate of 10.47%, which is about half a percentage point higher than the original rate. Our absolute winnings amounted to 471.27 rubles.

Obviously, with an increase in the amount or term of the deposit, the difference becomes even more noticeable.

Advantages and disadvantages of deposits with capitalization

It would seem that the conclusion is obvious: deposits with capitalization are more profitable than ordinary ones, and money should be placed only on compound interest terms.

However, not everything is so simple - it is not for nothing that simple deposits still prevail among the offers of most banks. There are several reasons for this state of affairs:

- Not all bank customers want to accumulate the received interest. Many consider them as a good addition to their monthly income and prefer to receive it on their current account.

- Often the conditions under which deposits with capitalization are opened do not provide for partial withdrawal of funds during the placement period. And such an opportunity is very attractive for many, since it leaves the right to take the bulk of the money in case economic instability or the occurrence of unforeseen difficulties.

- In most banks, the rate on deposits with capitalization is lower than when placing funds at a simple interest. The difference is often just the same 0.5 - 1%, which additionally brings capitalization. Therefore, when deciding on the choice of an investment program, one should proceed from a comparison of effective rates on deposits.

At the same time, a contribution with capitalization - effective and handy tool for those who have free funds and want to get on them maximum income. Among the main advantages of this type of accumulation are a convenient transparent scheme and pleasant sensations from constantly growing amounts of payments.

In conclusion, let us give some advice on choosing the method of placing financial resources in a bank, taking into account the topic of this article - the capitalization of interest.

- When choosing an accumulation strategy, it is necessary to take into account existing opportunities at the present time and assess possible needs in the near future. If you are sure that the available money will not be needed in the foreseeable future, you can look for a deposit with the highest effective rate, including the one obtained with the help of capitalization. If there is no such confidence, it may be worth sacrificing this option in favor of, for example, partial withdrawal - but keep in mind that most often when you terminate the bank deposit agreement early, you lose all the interest earned.

- In the process of choosing a specific program, it is necessary to analyze all the offers of the bank, both with and without interest capitalization. Comparison of the conditions for placing money should be carried out based on the size of the effective rate. Relevant information can be obtained from bank employees or as a result of calculations using deposit calculator on the website of the financial institution.

- No matter which type of deposit you prefer, Special attention should be given to the reliability of the bank. Information about this can be obtained from independent ratings, analysis of the structure of assets and the list of owners. Important factors are also the time of existence of the bank, its reputation and image. Well, it goes without saying that the organization to which you want to entrust your money must be part of the bank deposit insurance system, which provides state protection for all placed deposits up to 700 thousand rubles.

Almost always, the choice of a bank is a compromise between its reliability and the status and interest rate.

Thus, deposits with interest capitalization - great way to enlarge the rate valid at the time of opening the deposit for those who have money and want to invest it in order to maximize their savings. If the resulting effective rate on a deposit with capitalization is higher than with a regular placement, all other things being equal, feel free to accept the terms of such a deposit and get additional profit.

Source: http://predp.com/fin/money/kapitalizaciya-lada-chto-ehto.html

What is the capitalization of a deposit and the capitalization of interest on a deposit? Simple and Compound Interest

Modern banking system includes many financial and credit organizations whose work is based on competent management, such as own funds and attracted in the form of deposits.

Attracted may be free funds of individuals and legal entities, while the activity of attracting and the size of interest rates depend on how much the bank needs additional resources.

For example, the more non-paying customers a bank has, the more money it needs.

There are many types of deposits, but the most profitable for the client is such an investment free funds, at which the capitalization of interest on the deposit is provided. Therefore, when choosing a suitable type of deposit, one should clearly understand the meaning of 2 concepts: “deposit capitalization” and “deposit interest capitalization”.

Capitalization of the deposit

When drawing up an agreement for opening a deposit, a bank client does not have to face such difficulties as when applying for a loan, for example: providing a certificate of income or passing credit scoring, but he will definitely get acquainted with the "capitalization" parameter. What it is?

Capitalization of a deposit is an increase in its amount by the amount of accrued interest.

To explain more easily, this is the addition of interest to the balance of the contribution after a certain period of time.

During the capitalization of the deposit, interest is added to the amount of the deposit, which, upon expiration of its term, is transferred to the current account of the depositor. The calculation of interest during the capitalization of the deposit is each time based on the amount originally deposited, so their amount does not increase over time.

Types of capitalization of deposits depending on the conditions of placement:

- Annual- the most rare, it applies to long-term deposits. The amount of interest is calculated at the end of each year and is added to the deposit.

- Quarterly- occurs more often than the previous one. Interest is calculated every 3 months.

- monthly- interest is calculated at the end of each month.

- Daily- means the calculation of interest every day. It is classified as a temporary phenomenon, so it can be considered an exception.

- At the end of the term- interest is accrued once, after the expiration of the deposit, when the depositor receives money.

Example: let's say you have 100,000 rubles at 11% per annum.

The term of the deposit is 12 months. Let's take 2 years as an example.

According to the agreement, the accrual of interest is carried out at the end of the term (after 12 months). A new contract was concluded for the 2nd year (for the same amount and at the same percentage).

| 1 | 100 000,00 | 100 000,00 | ||

| 2-11 | 100 000,00 | 100 000,000 | ||

| 12 | 100 000,00 | 100 000,00 | ||

| Annual total: | 111 000,00 | 11 000,00 | 111 000,00 | 11 000,00 |

The annual yield of the deposit is 11,000 rubles. (100,000 rubles × 11% / 100% = 11,000). With the annual re-registration of the deposit, the income for 2 years will be 22,000.00 rubles. (11,000 × 2).

Simple interest

We have given the most simple example, the calculation of which will not be difficult. But what about the monthly, quarterly capitalization of the deposit when the contract is extended a large number of once? Here the simple interest formula comes to the rescue:, where:

- S

- I- annual interest rate;

- t- the number of days included in the period of accrual of interest on attracted deposits;

- K– number of days in a year (365 or 366);

- P- the initial amount of funds attracted to the deposit.

The sum of simple interest ( Sp) is calculated by the formula:

The simple interest formula is used if the interest accrued on a deposit is added to it either only at the end of the deposit term, or is not added at all, but is transferred to a separate account.

Example: suppose the bank accepted a deposit in the same amount as in the previous example - 100,000.00 rubles, but for a period of 30 days. The fixed interest rate is the same - 11% per annum.

Applying the formulas, we get the following results:

And now let's change the conditions a little: the bank took a deposit in the same amount, but for a quarter (90 days) with the same fixed rate - 11% "annual". Only the investment period has changed.

Comparing both examples, we see that the amount of monthly accrued interest remains unchanged:

Deposits with interest capitalization have some similarities and differences.

Interest in this case is also charged at the end of a predetermined period of time (year, quarter, month), but they are charged not on the “body” of the deposit, but on the “body” + previously accrued interest.

Capitalization of interest is the addition of interest to the amount of the deposit, which makes it possible to accrue interest on interest in the future.

In case of placement of funds with the possibility of capitalization of interest on the deposit accrued interest is not only added to the deposit amount, but also participate in further accrual.

This means that with each subsequent accrual, the amount of the deposit becomes larger by the amount of accrued interest.

As a result, interest is accrued on interest, due to which the effective rate on the deposit increases significantly.

Example: Let's take the initial data.

In the case of capitalization of interest on a deposit, the table will look like this:

| 1 | 100 000,00 | 111 000,00 | ||

| 2-11 | 100 000,00 | 111 000,00 | ||

| 12 | 100 000,00 | 111 000,00 | ||

| Annual total: | 111 000,00 | 11 000,00 | 123 210,00 | 23 210,00 |

At the time of the prolongation of the deposit for the 2nd year, its amount, taking into account the capitalization of interest, amounted to 111,000.00 rubles. The profitability of the deposit for 2 years amounted to 34,210.00 rubles. (11,000.00 + 23,210.00), including profitability only due to capitalization of interest compared to the previous option amounted to 12,210.00 rubles. (34,210.00 – 22,000.00 = 12,210.00).

Compound interest

The above example of calculating income on a deposit that provides for the capitalization of interest is as simple as possible. To calculate income under conditions of any complexity, apply compound interest formula:

,where:

- S- the amount of accrued funds that are due to be returned to the depositor upon the expiration of the deposit term: the initial amount of placed funds + accrued interest;

- I- annual interest rate;

- K- the number of days in a calendar year;

- J– the number of days in the period following which the bank capitalizes accrued interest;

- P- the initial amount of funds attracted to the deposit;

- n- the total number of interest capitalization operations for the entire period of raising funds.

The compound interest formula is used if interest on the deposit is accrued at regular intervals(every month, every quarter), that is, the calculation provides for the capitalization of interest (when interest is accrued on interest).

An example of how to calculate compound interest and the amount of a bank deposit with compound interest. The bank took a deposit in the amount of 100,000.00 rubles. for a quarter (90 days) with the same as in the previous examples, a fixed rate - 11% "annual" and with monthly interest. This means that in 90 days 3 (90:30) transactions will be made to capitalize the accrued interest. So, we have the following data: I= 11%; K= 365 days; J= 30 days; P= RUB 100,000.00; n = 3 periods. What will be the amount of interest (Sp)? Now let's determine the amount of this deposit:

S \u003d P + Sp \u003d 100,000.00 + 2736.93 \u003d 102,736.93 rubles.

Let's check the correctness of the calculation using the compound interest formula:

And now let's compare the income for the same period and with the same interest rate (3 months, 11% per annum) in the case of simple and compound interest. In the first case, the amount of the deposit amounted to 102,712.33 rubles.

And in the second - 102,736.93 rubles. As you can see, there is a slight discrepancy in favor of interest capitalization (compound interest).

If the capitalization period and, accordingly, the number of periods is longer, then the difference will become noticeably more noticeable, as can be seen from the graph below.

conclusions

If we compare deposits that imply periodic interest payments and deposits with interest capitalization, then the advantage of the latter is more high level income. Such a profitable placement of free funds is an ideal option for clients who do not want to withdraw interest at the end of the month (quarter, year).

Those who wish to learn how to produce more complex financial calculations, you need to familiarize yourself with the six functions of compound interest.

As for the topic described in this article, a deposit with a monthly interest capitalization and a low interest rate is more profitable than a deposit that implies a high interest rate, but with interest accrued, for example, once every six months.

Real income for a specific period and the interest rate are different things, so you need to objectively evaluate the tempting and high interest rates on deposits.

What is the capitalization of the contribution and 3 disadvantages of capitalization. What may affect the conditions of a bank deposit? What are the terms for calculating interest on a deposit? How to choose a profitable bank deposit?

A deposit is one of the most common ways to store money.

In order for the amount not only to lie at home, under the mattress, but, it is usually put in financial institution under a certain percentage.

Thus, capital is partially insured against depreciation. Or at least it is stored in safe place, and all the time is "in work".

There are different deposits, and each bank offers its own conditions. Usually, the choice of conditions depends on the term and purpose of such investments.

One of the not unimportant characteristics of a bank deposit is the periods in which the client can make a profit, this is what defines the concept, what is capitalization of a deposit.

Capitalization of the deposit - what is it?

What is the capitalization of a contribution in simple terms?

Capitalization of a deposit is a type of calculation and accrual for the amount that was deposited into the account.

More precisely - the accrual of income not at the end of the selected period, from the initial amount, but throughout the entire period at certain stages.

For example, quarterly, when the dividend is accumulated in stages, four times a year. Each time it is calculated not from the initial amount, but from the one to which a certain share has already been accrued.

To make it more clear, you can parse this with an example:

Let's take an initial capital of 1,000,000 rubles, which was deposited in a bank, at 12% per year.

At the same time, we will choose the rate of monthly crediting on the deposit. Every month, the amount in the account will increase by 1%.

In the first month, 10,000 rubles will “fall” into the account. As a result, we get 1,010,000.

AT next month 1% will also be charged, but it will no longer be 10,000, but 10,100.

And so on every month.

The general formula by which the transfers are made looks like this:

For example, the same 100,000 rubles, and if we take interest rates of 10%, 15% or 20%.

In half the cases, choosing the type of investment with the condition of monthly crediting to the account, but not with such a high percentage, you can get more than in the case of the annual accrual, but with a higher bank rate.

"Pros and cons" of capitalization of deposits

The advantages of such a proposal would seem to be obvious. At a minimum, we saw this in the example above.

However, as in many other financial situations, there are some drawbacks.

Among the minuses, the following points can be distinguished:

- In case of premature withdrawal of investments in full (termination of the contract for a certain duration), the investor receives a completely different dividend, which depends on the current accounts in the selected institution.

Even if credits occur frequently, they can be withdrawn only in certain deadlines specified in the contract.

But this is a dubious minus, since it confuses not everyone.

Compound interest is not always more profitable than the standard method of calculating the income rate, since such a rate is usually lower, so it is not always worth choosing a deposit with a complex calculation.

It is better to analyze all offers and choose the most profitable one, which will allow you to get the most.

Where else can capitalization and its types occur?

1. On a loan (credit).

Of course, in the case of bank investments, compound interest works to the advantage of the depositor, if he correctly calculated and understood the conditions.

But sometimes such a factor as capitalization is not positive. For example, in the case of lending.

Often there is such a situation when a person takes not such a huge amount, but pays it for a very long time. During this period, it would be possible to repay the debt in full a long time ago, however, sometimes only half is repaid.

This is where compound interest comes in.

In this situation, the following picture is obtained: every month the initial amount grows by a certain percentage. What does it mean - the overpayment is calculated from the amount with the interest already accrued.

This is far from the most profitable terms lending, since in this case the overpayment can be reduced only by paying off the debt as soon as possible.

2. On the market (market).

This process can be traced almost everywhere in the economy, for example, in the market.

If we are talking about market capitalization, then we can consider the calculation money growth a certain area of the economy, industry, or even a single company.

If you choose the activity of a certain enterprise, then, with the help of its accounting report, you can see the increase or decrease working capital of this firm.

In order to get the true picture, it is necessary to take into account only the capital owned by the enterprise itself, excluding all borrowed funds from calculations.

Market capitalization has nothing to do with deposits, but it reflects General characteristics this process.

How to choose the optimal conditions for bank investments?

What are the periods for crediting dividends on a deposit?

All the intervals through which the bank credits income are selected and offered by the bank itself. The depositor accepts or rejects the conditions offered by the bank.

There are such periods of accrual of income at the rate:

- One-time credit- the most unprofitable capitalization, since, in fact, there are no internal accruals, only at the end of the deposit period.

- Monthly capitalization- the most suitable for a short deposit period, as the interest drops every month.

- Daily is a very rare occurrence, since this type of deposit will be very profitable for the depositor, but very unprofitable for the bank.

Enrollment annually- brings insignificant income, if we are talking about a short period of time (2-3 years).

If we consider a longer period (for example, from 5 years), it can turn out to be a very profitable solution.

Quarterly capitalization– this option is more profitable and convenient for those who are interested in a short-term deposit.

The reason is that a certain percentage, according to the rate, will drip every 3 months.

What are the main points to pay attention to?

After analyzing all the offers and benefits, have you already decided that the type of deposit with compound interest growth is right for you?

Still, you need to take into account additional nuances that may affect how profitable this deposit will be.

List of nuances that should always be discussed with a bank employee:

- What will be the interest rate if capitalization is not taken into account?

- Terms and periods of accruals on the amount of investment.

- How will interim interest be calculated?

You need to understand that interim dividends can be credited to a separate account, which means that the initial deposit amount will not change during the selected period.

And at the end of the period, only the total interest on the deposit from the original amount is charged.

Or, as in the calculations above, intermediate charges can be added to the initial capital and, as a result, a further percentage will be calculated from the total amount.

Conclusion on what is the capitalization of the contribution and the short advantage

From the foregoing, we can conclude that such a phenomenon as capitalization still has more pluses than minuses.

This type of investment is designed for those people who are interested in income stability, as well as the desire to receive maximum amount for the shortest period.

If we are talking about raising money for the purpose of buying real estate or other high-cost purposes, then the deposit, which takes into account investment capitalization is exactly what is needed.

However, there are areas in which it is not only a positive moment. One of them - . Interest capitalization in lending is also growing rapidly, as well as interest in a long-term deposit.

Just about the complex. What is the capitalization of a deposit?

How it works? Details in the video:

However, in the case when a deposit with capitalization is decisively chosen, you need to carefully select the conditions, since it is very difficult to find a bank that offers high percent on fair terms...

Useful article? Don't miss out on new ones!

Enter your e-mail and receive new articles by mail